RF Components Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

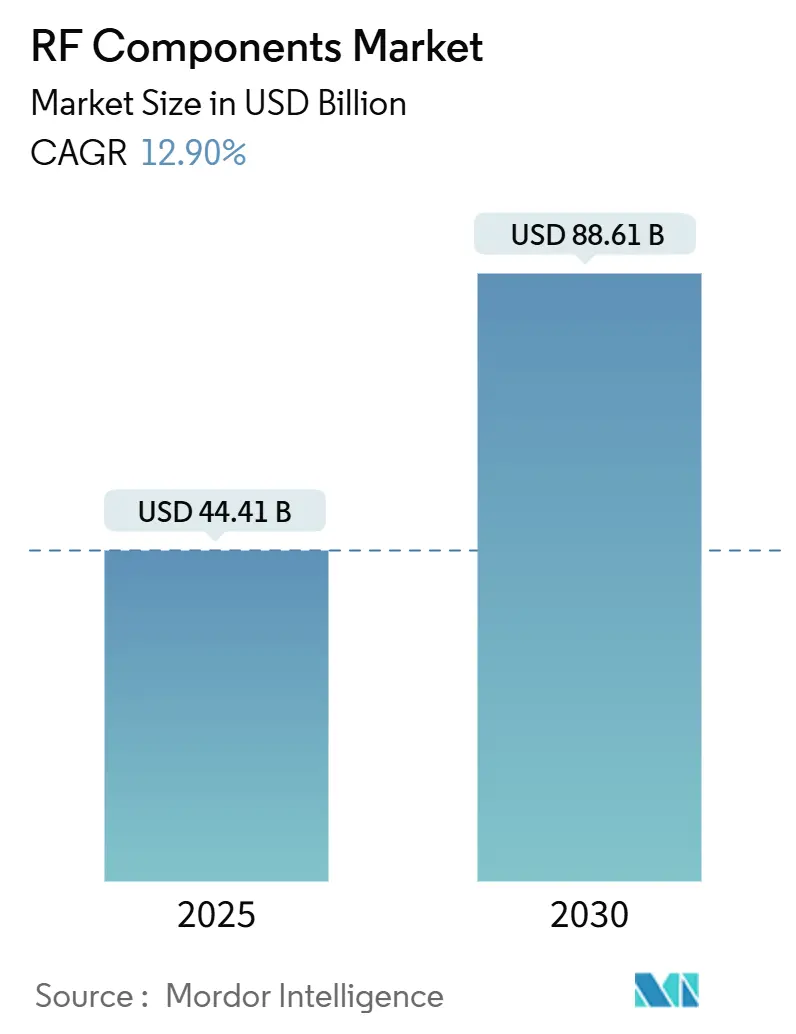

| Market Size (2025) | USD 44.41 Billion |

| Market Size (2030) | USD 88.61 Billion |

| Growth Rate (2025 - 2030) | 12.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

RF Components Market Analysis by Mordor Intelligence

The RF components market size stands at USD 44.41 billion in 2025 and is projected to reach USD 88.61 billion by 2030, expanding at a 12.9% CAGR over the forecast period. The growth path reflects surging deployments of 5G base stations, radar-centric autonomous vehicles, and space-based communications platforms. Government programs that localize semiconductor supply chains, breakthroughs in frequencies above 40 GHz, and rising content per smartphone collectively reinforce demand momentum. Competitive strategies emphasize vertical integration, AI-assisted design automation, and advanced thermal packaging, opening opportunities for suppliers able to balance performance and cost while navigating geopolitical headwinds. The RF components market also benefits from policy-driven investments in Open RAN, low-Earth-orbit (LEO) constellations, and edge-AI industrial automation, all of which require frequency-agile, power-efficient architectures.

Key Report Takeaways

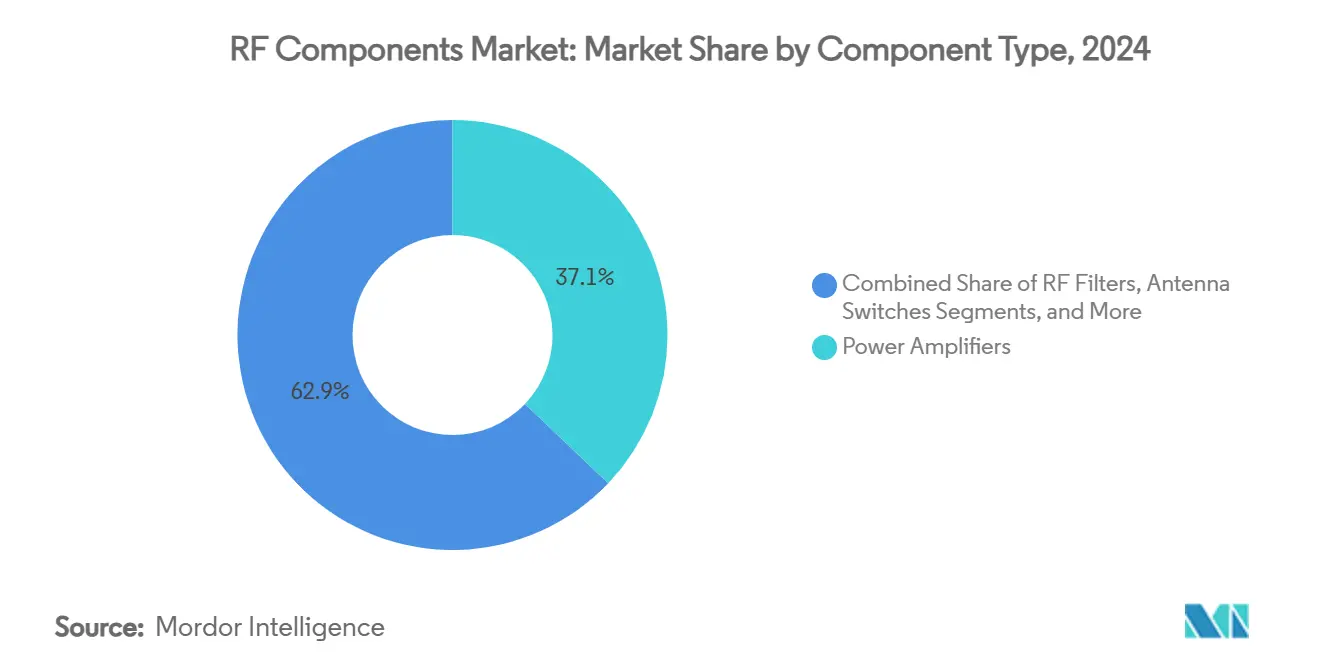

- By component type, power amplifiers held 37.1% of RF components market share in 2024, while RF tunable devices are forecast to expand at a 14.1% CAGR through 2030.

- By frequency band, Sub-6 GHz accounted for 62.5% share of the RF components market size in 2024; the 40-100 GHz band is advancing at a 13.9% CAGR to 2030.

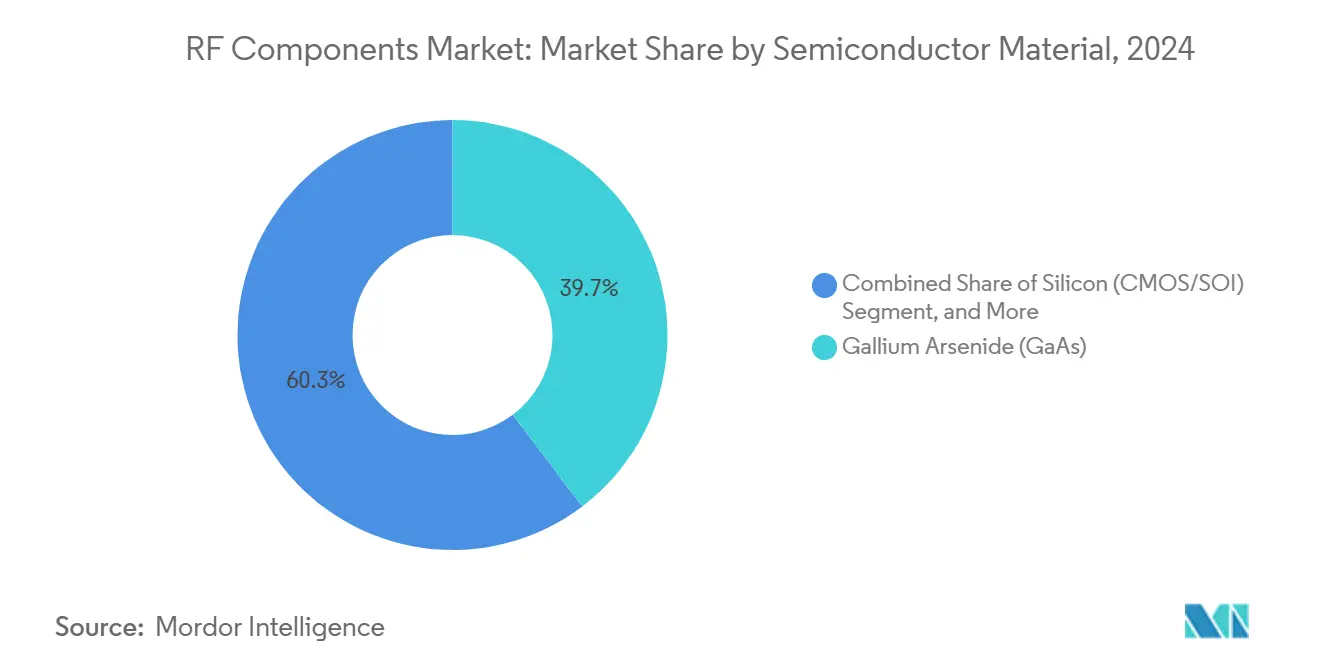

- By semiconductor material, GaAs led with 39.7% share in 2024, whereas GaN solutions are projected to grow at a 13.8% CAGR between 2025-2030.

- By end-user industry, consumer electronics captured 51.4% of the RF components market size in 2024 and automotive applications are rising at a 14.3% CAGR through 2030.

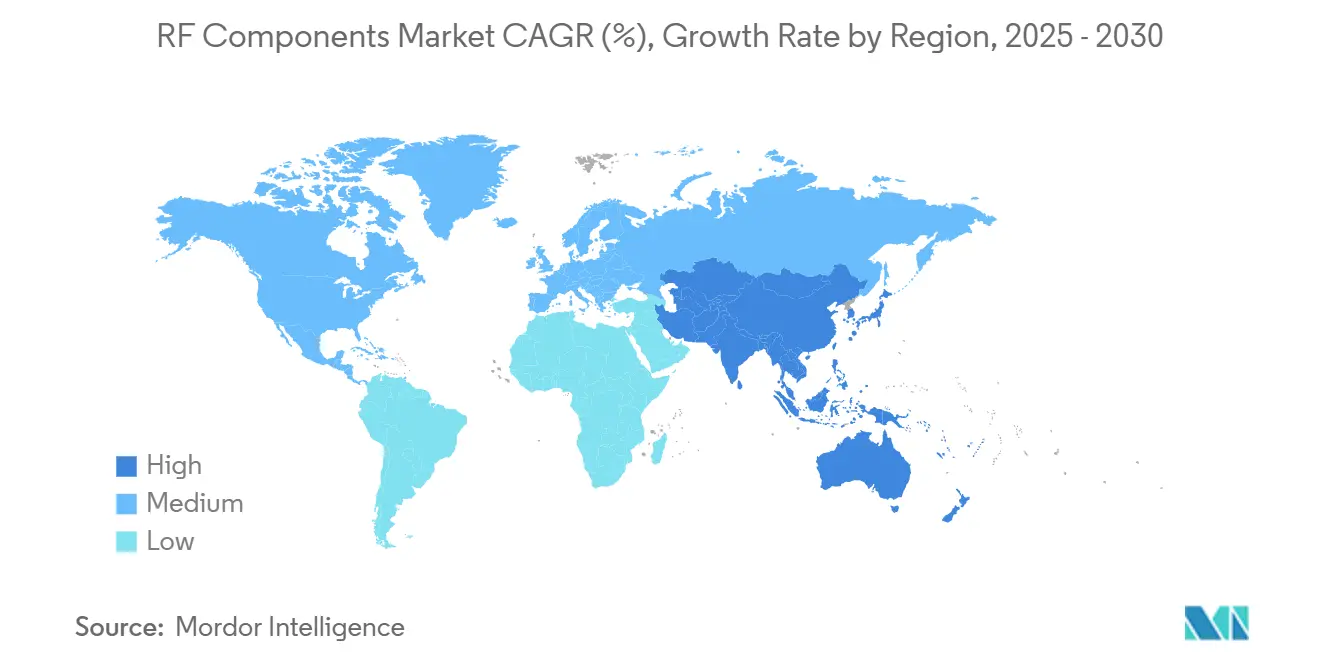

- By geography, Asia-Pacific commanded 56.2% revenue share in 2024; North America records the fastest regional investment growth at 14.2% CAGR on the back of CHIPS Act incentives.

Global RF Components Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G infrastructure densification | +3.2% | Global; APAC & North America lead | Medium term (2-4 years) |

| Surge in RF front-end content per smartphone | +2.8% | APAC manufacturing hubs | Short term (≤ 2 years) |

| Rising automotive radar & V2X deployments | +2.5% | North America & EU regulations | Medium term (2-4 years) |

| Government funding for space & LEO constellations | +1.9% | North America & EU with APAC spillover | Long term (≥ 4 years) |

| Rapid adoption of RF energy-harvesting PMICs | +1.4% | Early adoption in North America & EU | Medium term (2-4 years) |

| Edge-AI mmWave sensing in smart-factory cobots | +1.1% | APAC, exping to North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Infrastructure Densification Drives Macro-Cell RF Dem

Mobile operators continue to densify 5G macro-cell networks, requiring high-efficiency power amplifiers, low-loss filters, and beam-steering switches that can withstand elevated thermal loads. The strategy is reinforced by Open RAN programs, notably the USD 450 million Public Wireless Supply Chain Innovation Fund, which incentivizes multi-vendor interoperability software-defined architectures.[1]National Telecommunications Information Administration, “Biden-Harris Administration Awards USD 117 Million for Wireless Innovation,” ntia.gov Partnerships such as MaxLinear RFHIC’s 55.2%-efficiency GaN power amplifier underline the focus on energy savings for large-scale deployments. As macro cells deliver higher power than small cells, suppliers with GaN process maturity gain a competitive edge. Policy support through 2027 ensures a sustained dem runway, giving the RF components market a strong anchor for mid-term revenue visibility.

Automotive Radar Integration Accelerates V2X Ecosystem Development

Each Level-3-ready vehicle now carries multiple 77-81 GHz radar sensors alongside dedicated V2X transceivers, doubling RF content per unit compared with 2023 models. North American and European regulators require advanced driver-assistance systems (ADAS) to meet functional safety norms, nudging OEMs toward fully qualified automotive-grade RF suppliers.[2]U.S. Department of Homel Security, “5G Impacts to Vehicles Highway Infrastructure,” dhs.gov ISO 26262 certification and FCC Part 15 compliance further restrict sourcing to vendors with proven reliability records. The dual use of radar V2X intensifies design complexity, boosting dem for integrated front-end modules that balance isolation and coexistence. Lead times for high-Q dielectric materials remain elevated, posing short-term supply risks yet reinforcing premium pricing for qualified inventories.

Government Space Funding Catalyzes LEO Constellation RF Innovation

Space agencies' defense departments fund wide Ka- Ku-b payloads, allocating multi-year budgets that stabilize long-cycle revenue. The U.S. Space Force and UK Space Agency initiatives prompt suppliers like MACOM to launch radiation-tolerant Q-b power amplifiers and opto-amp families.[3]MACOM Technology Solutions, “MACOM Launches High Power Opto-Amp Series at SATELLITE 2025,” stocktitan.com LEO operators favor software-defined radios capable of in-orbit frequency agility, which in turn propels RF tunable device adoption. Space-grade qualification stretches 18-24 months, creating high entry barriers but cementing long-term supplier relationships once passed.

mmWave Thermal Management Creates Technical Differentiation

Operating above 28 GHz elevates junction temperatures, with studies showing 68°C peaks within 10 seconds, a 21% drop in throughput, making thermal design a core competitive parameter. Suppliers invest in embedded heat-spreader substrates and high-conductivity interface materials to retain performance while shrinking package footprints. Military aerospace specifications, anchored in IEC 60068 thermal cycling, raise the bar further. Vendors that master thermal-aware packaging consolidate share in the upper-mmWave domain, an area expected to proliferate as 6G prototypes progress.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for GaN/GaAs wafer fabs | -2.1% | Global; challenges new entrants | Long term (≥ 4 years) |

| Thermal-management challenges above 28 GHz | -1.8% | Global; mmWave-centric segments | Medium term (2-4 years) |

| Export-control tightening on ultra-wideb chips | -1.5% | US-China supply corridor | Short term (≤ 2 years) |

| Shortage of high-Q dielectric materials | -1.2% | APAC manufacturing concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX Requirements Limit GaN/GaAs Fab Expansion

A new compound-semiconductor line can cost USD 2-5 billion, underscored by TSMC’s Arizona outlay that eclipses USD 165 billion when fully built.[4]SEMI Vision, “TSMC’s Arizona Plant Presses Fast-Forward on Expansion,” substack.com Even with CHIPS Act incentives, smaller entrants struggle to secure financing for molecular-beam epitaxy MOCVD tools. MACOM’s USD 180 million expansion, subsidized by federal backing, illustrates how government aid can offset but not erase capital hurdles. The multiyear build--qualify cycle delays market entry, encouraging consolidation, and favoring incumbents with depreciated assets.

Shortage of High-Q Dielectric Materials Constrains Production

Fabricators of multi-layer ceramic capacitors (MLCCs) prioritize high-volume smartphone dielectrics, leaving radar-grade, high-Q formulations in short supply. Lead times extend to six months, affecting filter tuner output critical for ADAS satellite terminals. Raw-material concentration in Japan and South Korea adds geographic risk, and REACH compliance in Europe complicates substitution. The limitation is expected to ease slowly as more capacity comes online post-2026, yet it remains a medium-term drag on the RF components market.

Segment Analysis

By Component Type: Power Amplifiers Underpin Share While Tunable Devices Accelerate

Power amplifiers generated the largest slice of the RF components market in 2024, accounting for USD 16.5 billion. Their entrenched role in macro-cell radios, radar modules, home-gateway equipment anchors volume dem, even as efficiency mates intensify. Meanwhile, RF tunable devices compound at 14.1% annually through 2030. Enterprises adopt these components to enable seamless cross-b transition, especially in Open RAN LEO terminals, where software-defined architectures streamline network upgrades. Qualcomm’s X85 modem-RF platform integrates an AI engine that dynamically tunes filters and switches, highlighting the march toward smarter front ends. Suppliers that merge power amps, low-noise amps, and tuners into single modules help customers shrink board area while easing thermal budgets, a trend visible in Qorvo’s latest Wi-Fi 7 front-end modules.

Second-order effects reinforce this trajectory. Higher-order MIMO topologies in 5G NR Release 18 boost the number of signal paths per base station, multiplying power-amplifier sockets even when per-path wattage tapers. In smartphones, antenna-switch multiplexing rises with 5G STBY modes that leverage non-contiguous carrier aggregation, driving RF switch shipments. Integrated filter-switch banks support coexistence across Sub-6 GHz spectra, preserving linearity while containing BOM costs.

Note: Segment shares of all individual segments available upon report purchase

By Frequency Band: mmWave 2 Gains Traction on Ultra-High-Speed Links

The Sub-6 GHz domain still owns 62.5% of the RF components market share thanks to the sheer footprint of LTE early 5G radios. However, the 40-100 GHz band grows the fastest at a 13.9% CAGR, favored by enterprise fixed-wireless access (FWA), backhaul links, and emerging 6G research corridors. NTIA’s public consultation on 6G use cases underscores governmental intent to leverage these higher bands for next-generation gigabit services. Suppliers adept at thermal-conscious packaging position themselves to capitalize on this incremental wave. The 24-40 GHz class observes steady, yet slower, adoption in dense urban mmWave 5G—thermal design, siting logistics, and backhaul costs temper mass rollout velocity.

Technical maturation drives competitive behavior. Beam-steering ICs with embedded phase shifters shrink the antenna aperture needed for data-center roof links, while GaN-on-SiC power amplifiers unlock higher EIRP at manageable drain voltages. Regulatory alignment, such as the FCC’s millimeter-wave service rules, fosters certainty but still demands sophisticated coexistence management with satellite incumbents.

By Semiconductor Material: GaN Surges on Power-Efficiency Demands

While gallium arsenide continues to lead in base volume, gallium nitride (GaN) is making significant inroads, thanks to its superior electron mobility. GaN's reach has expanded from macro-cell radios to electric vehicle chargers. The market for RF components utilizing GaN devices is set to see its size double between 2025 and 2030. Geopolitical tensions in the supply chain are a concern; for instance, China's export restrictions on gallium are pushing Western manufacturers to not only diversify their mining sources but also to ramp up recycling efforts. Initiatives in the U.S. to stockpile materials, coupled with the EU's alliances for raw materials, are helping to cushion these geopolitical shocks. On another front, while silicon-based CMOS RF technologies maintain a cost advantage in consumer multi-band IoT applications, they encounter performance limitations beyond the 6 GHz mark. Meanwhile, silicon-germanium combinations are finding their sweet spot in radar applications, striking a balance between low noise and moderate cost.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Automotive Radar Drives Growth Acceleration

In 2024, consumer electronics led in unit shipments, yet their growth has tapered to single digits. In contrast, the automotive sector is expanding at a faster pace than any other, with projections indicating a rise in radar sensors from two to six per vehicle, coupled with V2X connectivity in North America by 2028. Studies by DHS underscore the importance of robust RF design for ensuring traffic safety. The telecommunications sector, buoyed by densified 5G and early 6G testbeds, stands as the second-fastest growing domain. Meanwhile, industrial automation is integrating edge-AI sensing at mmWave frequencies, enhancing robotic precision and safety in smart factories. The aerospace defense sector maintains a steady high-margin niche, dominated by ruggedized and radiation-hardened components.

Geography Analysis

In 2024, Asia-Pacific dominated the RF components market, claiming a 56.2% share. This surge was largely fueled by the inauguration of 18 new fabs in China alone. Government subsidies have effectively reduced unit costs, and the region's proximity to key OEMs has bolstered visibility. While South Korea and Japan continue to lead in substrate materials and filter ceramics, Taiwan's foundries are at the forefront, providing advanced packaging for multichip modules. India's push for 5G, backed by the Production-Linked Incentive (PLI) scheme, is drawing backend assembly operations, though the country currently lacks a significant wafer-fab scale. Even with rising trade restrictions, Asia-Pacific's cost advantages ensure it anchors over half of the global shipments for the foreseeable decade.

North America is riding the wave of the CHIPS Act. TSMC's facility in Arizona is not only introducing 4-nanometer class processes but also bringing advanced RF packaging closer to U.S. clients. This move significantly reduces logistics risks, bolstering the security of defense supply chains. Additionally, federal grants amounting to USD 117 million, sourced from the wireless innovation fund, are championing domestic Open RAN radio development, steering business towards American RF specialists. While Canada is upgrading its telco infrastructure for mid-band 5G, it predominantly relies on U.S. component imports. Meanwhile, Mexico's EMS sector is capitalizing on low-cost assembly contracts for customer premises equipment (CPE) devices.

Europe, eyeing a 20% share of the global semiconductor market by 2030, is positioning itself for strategic autonomy through the European Chips Act. In Germany and France, automotive OEM clusters are anchoring radar modules to meet Euro NCAP safety standards, boosting local fab utilization. The UK's GBP 16 million LEO program is backing Ka-band component R&D, nurturing a nascent space supply chain. Nordic nations are experimenting with millimeter-wave fixed wireless access for rural broadband, procuring GaN front-end equipment from U.S. and Japanese suppliers. However, regulatory challenges, such as the REACH chemistry rules, are extending part qualification cycles, inadvertently benefiting established players with a history of European compliance.

Competitive Landscape

In the RF components market, the top five vendors command the majority of the revenue, striking a balance between scale efficiencies and dynamic specialist innovation. Leading the charge in 2024 is Broadcom, boasting a semiconductor turnover of USD 30.1 billion, seamlessly integrating Wi-Fi, cellular, and broad RF chips into its expansive networking portfolio. Skyworks, while facing unit declines, adeptly maintains its foothold in premium smartphones by capitalizing on a higher average content per device. Qorvo pushes the envelope on module integration, as showcased by its Wi-Fi 7 front-end, which condenses power, LNA, and filtering into a footprint that's 30% smaller. Meanwhile, emerging players, buoyed by the USD 30 million AIDRFIC program, harness AI design flows to accelerate tape-outs, posing a challenge to established firms in niche markets.

Strategic maneuvers highlight a trend of deliberate capability enhancement. In 2024, Qorvo's acquisition of beam-forming expert Anokiwave expands its mmWave array offerings. Concurrently, onsemi's foray into silicon-carbide technology bolsters its high-voltage expertise, a boon for EV chargers. Distribution partnerships, like Mouser's alliance with Ampleon, amplify market reach for GaN power components, especially in 5G broadcast towers. The competitive landscape is increasingly defined by thermal packaging patents, programmable RF front-ends, and the secure domestic supply credentials that defense clients prioritize.

Reshoring initiatives are reshaping cost dynamics. Customers in the U.S. and EU are turning to local test-and-assembly services, aiming to navigate the complexities of cross-border export-control scrutiny. In response to rising labor costs, vendors are doubling down on automation and volume commitments. Looking ahead, suppliers who can seamlessly integrate global fabrication networks with a keen understanding of regional customer needs stand poised to seize a significant share of the RF components market.

RF Components Industry Leaders

-

Broadcom Inc.

-

Skyworks Solutions Inc.

-

Qorvo Inc.

-

Murata Manufacturing Co., Ltd.

-

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Murata introduced the first XBAR-based high-frequency filter spanning 5 150-7 125 MHz.

- June 2025: Mouser signed a global distribution agreement with Ampleon for GaN LDMOS RF power parts.

- March 2025: Qualcomm unveiled the X85 5G Modem-RF at MWC Barcelona 2025, integrating AI processing for peak 12.5 Gbps downloads.

- March 2025: MACOM launched its High Power Opto-Amp series, adding linearized Q-b power amplifiers aimed at LEO constellations.

- February 2025: MaxLinear RFHIC delivered a 55.2%-efficient GaN power amplifier for 5G macro radios.

Global RF Components Market Report Scope

The RF module is used to transmit and/or receive radio signals between two devices through several market components, such as power amplifiers and antenna switches, integrating into applications like consumer electronics and automotive.

| By Component Type | Power Amplifiers | |

| RF Filters | ||

| Antenna Switches | ||

| Low-Noise Amplifiers | ||

| RF Tunable Devices | ||

| By Frequency Band | Sub-6 GHz | |

| 6-24 GHz (C/X/Ku) | ||

| 24-40 GHz (mmWave 1) | ||

| 40-100 GHz (mmWave 2) | ||

| By Semiconductor Material | Gallium Arsenide (GaAs) | |

| Silicon (CMOS/SOI) | ||

| Gallium Nitride (GaN) | ||

| Silicon-Germanium (SiGe) | ||

| By End-User Industry | Consumer Electronics | |

| Telecommunication | ||

| Automotive | ||

| Aerospace and Defense | ||

| Industrial Automation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| Power Amplifiers |

| RF Filters |

| Antenna Switches |

| Low-Noise Amplifiers |

| RF Tunable Devices |

| Sub-6 GHz |

| 6-24 GHz (C/X/Ku) |

| 24-40 GHz (mmWave 1) |

| 40-100 GHz (mmWave 2) |

| Gallium Arsenide (GaAs) |

| Silicon (CMOS/SOI) |

| Gallium Nitride (GaN) |

| Silicon-Germanium (SiGe) |

| Consumer Electronics |

| Telecommunication |

| Automotive |

| Aerospace and Defense |

| Industrial Automation |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

Key Questions Answered in the Report

How large will the RF components market be by 2030?

It is forecast to reach USD 88.61 billion, nearly doubling from 2025 at a 12.9% CAGR.

Which component type is growing fastest?

RF tunable devices lead growth with a projected 14.1% CAGR through 2030 due to dem for frequency agility in 5G satellite links.

Why is GaN adoption accelerating?

GaN delivers higher power density efficiency, making it vital for 5G macro cells EV charging, driving a 13.8% CAGR for GaN devices.

Which region dominates supply?

Asia-Pacific accounts for 56.2% revenue in 2024, anchored by extensive foundry capacity proximity to hset OEMs.

What limits mmWave deployment?

Above 28 GHz, thermal loads escalate, deming advanced packaging; insufficient heat removal can cut data throughput by over 20%.

How are governments influencing the sector?

Programs like the U.S. CHIPS Act NTIAs USD 450 million Open RAN fund channel capital into domestic fabs open-stards radio components, reshaping global supply patterns.

Page last updated on: