Market Overview

| Study Period | 2020 - 2030 |

|---|---|

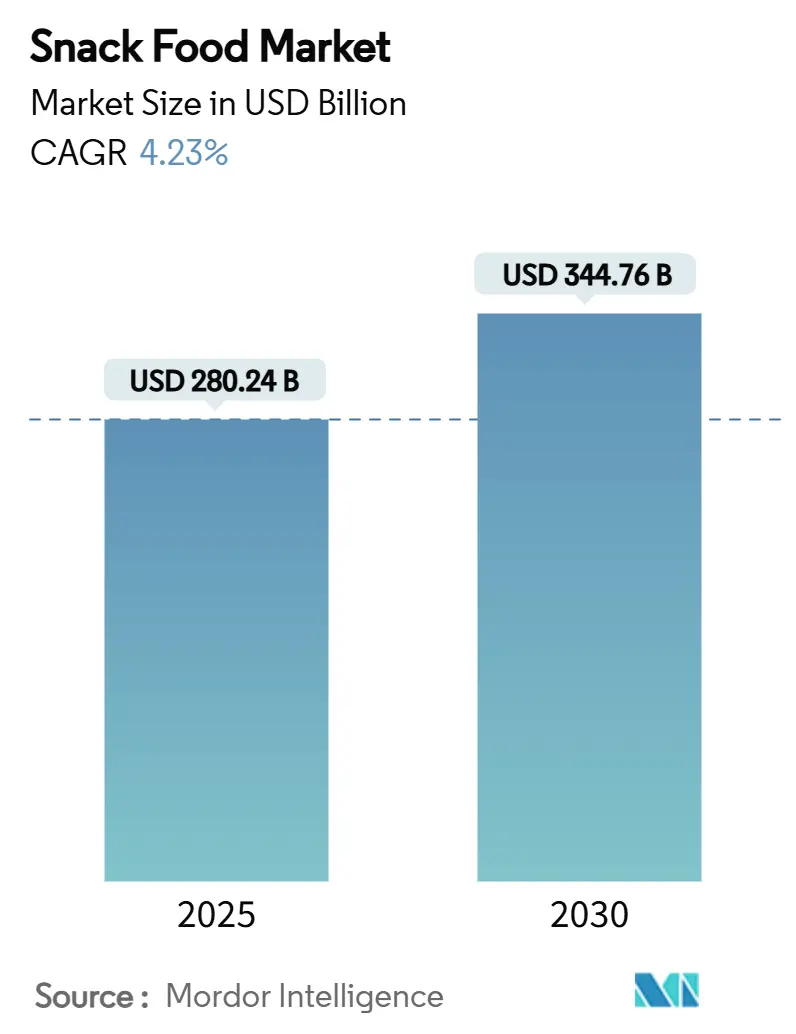

| Market Size (2025) | USD 280.24 Billion |

| Market Size (2030) | USD 344.76 Billion |

| Growth Rate (2025 - 2030) | 4.23% CAGR |

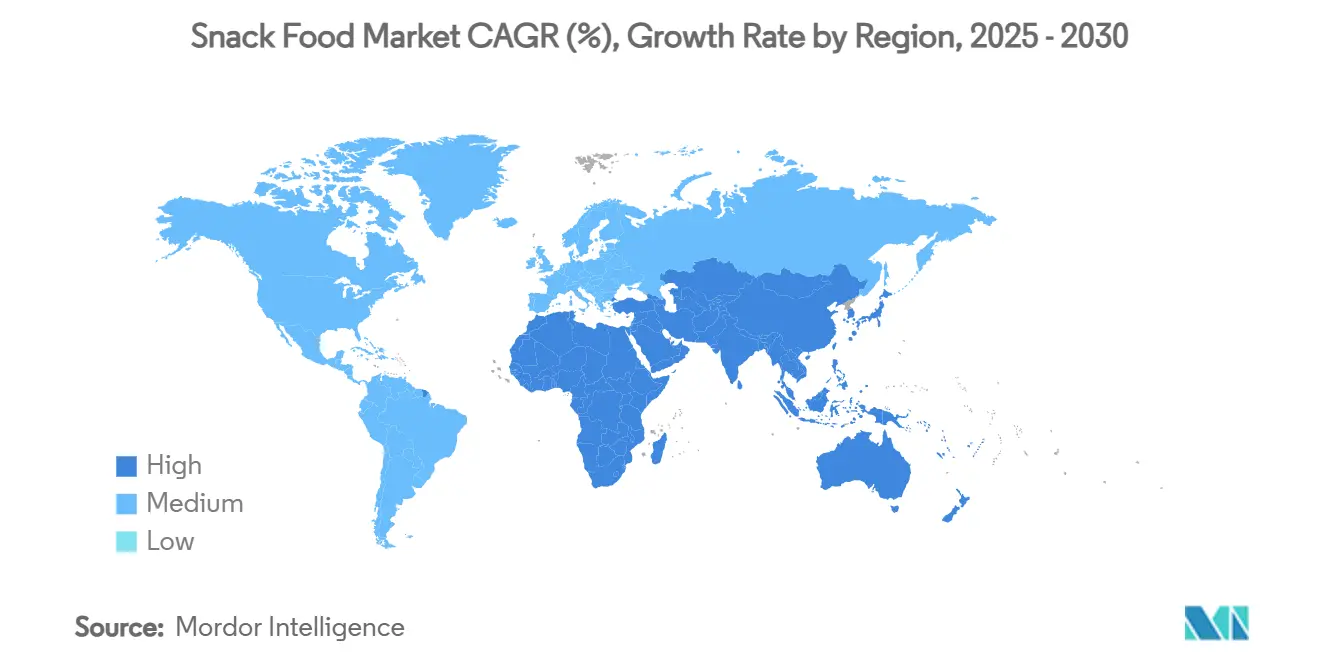

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Snack Food Market Analysis by Mordor Intelligence

The snack foods market size stood at USD 280.24 billion in 2025 and is projected to reach USD 344.76 billion by 2030, reflecting a 4.23% CAGR over the forecast period. Convenience continues to be a significant driver of demand, with 92% of adults reporting at least one snacking occasion within a 24-hour period. This underscores the increasing consumer preference for accessible and ready-to-eat options that fit into their busy lifestyles. Digital commerce, combined with quick-commerce fulfillment models, is transforming route-to-market strategies by enabling faster delivery, expanding brand visibility, and leveraging data-driven personalization to meet diverse consumer needs effectively. At the same time, regulatory and sustainability agendas are gaining momentum. Key initiatives, such as HFSS advertising restrictions aimed at curbing the promotion of high-fat, salt, and sugar products, and extended-producer-responsibility mandates focusing on sustainable waste management, are driving investments toward the development of healthier product formulations and innovative, low-impact packaging solutions[1]Source: United Kingdom Government,"Restricting advertising of less healthy food or drink on TV and online: products in scope", www.gov.uk. These shifts reflect the growing alignment of industry practices with consumer expectations and regulatory requirements.

Key Report Takeaways

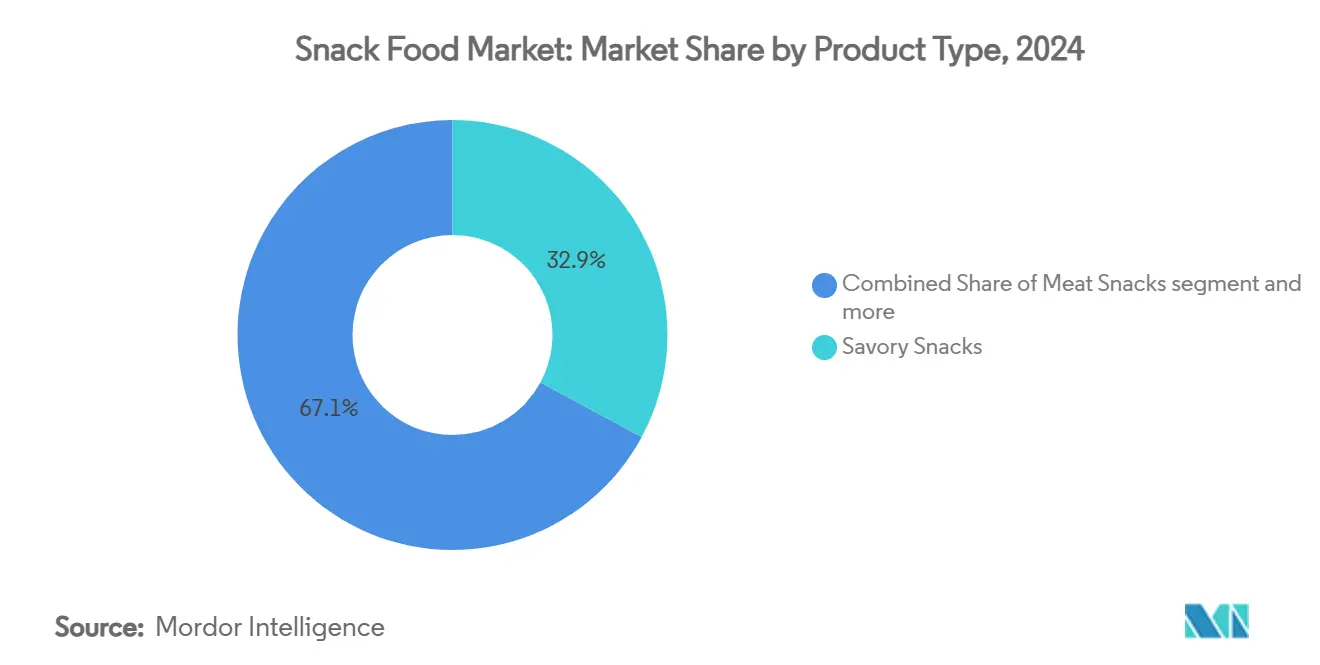

- By product type, savory snacks led with 32.87% market share in 2024, whereas meat snacks are poised to post a 6.26% CAGR through 2030.

- By ingredient type, conventional recipes held 63.54% share in 2024, while organic / clean-label lines are projected to record a 5.35% CAGR over 2025–2030.

- By distribution channel, supermarkets/hypermarkets captured 34.68% of the 2024 base, and online retail is projected to register a 5.64% CAGR through 2030.

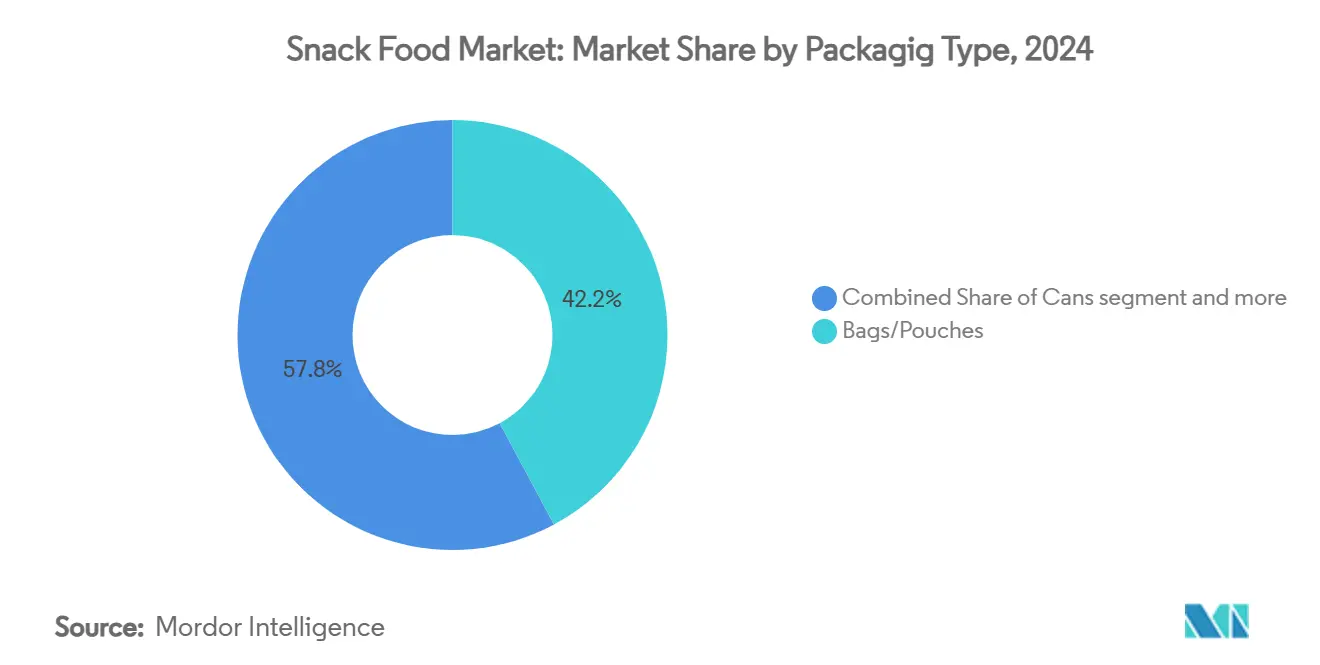

- By packaging type, bags/pouches commanded 42.17% share in 2024, and cans are forecast to log 4.63% CAGR as brands pursue circular-ready formats.

- By geography, Asia-Pacific contributed 31.68% of global sales in 2024 and Middle East and Africa is anticipated to be the fastest climber at 4.83% CAGR to 2030.

Global Snack Food Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient foods | +1.2% | Global with peak effect in North America and Asia-Pacific | Medium term (2–4 years) |

| Growing demand for fortified and functional snacks | +0.9% | North America and Europe expanding into Asia-Pacific | Long term (≥ 4 years) |

| Expansion of snackification as meal replacements | +0.8% | Urban centers worldwide | Medium term (2–4 years) |

| Growing penetration of e-commerce and quick-commerce | +0.7% | Global with rapid momentum in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Upcycling food waste into value-added snacks | +0.4% | North America and Europe and emerging in Asia-Pacific | Long term (≥ 4 years) |

| Flavor forward localization | +0.3% | Global with regional flavor nuances | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient foods

Urban lifestyles are shrinking meal times, driving up demand for portable, individually portioned packs. Brands are increasingly adopting resealable pouches and oxygen-barrier films, which not only extend shelf life but also cater to the needs of on-the-go consumers. These packaging innovations ensure convenience while maintaining product freshness, making them highly appealing to busy urban populations. This trend leans heavily towards protein-rich offerings, particularly in meat and plant-protein categories, as they provide meal-replacement satisfaction and meet the growing consumer preference for high-protein diets. The rise of quick-commerce further amplifies this trend, favoring companies that can efficiently deliver high-demand SKUs within a 15-minute window, a critical factor in maintaining competitiveness in this fast-paced market. Meanwhile, manufacturers face the challenge of adhering to stringent labeling standards, which require them to ensure that their formulations, packaging designs, and claims comply with FDA nutritional disclosure mandates, adding another layer of complexity to product development and marketing strategies.

Growing demand for fortified and functional snacks

Consumers are increasingly shifting from empty-calorie snacks to those rich in protein, fiber, probiotics, and essential micronutrients, driven by a growing awareness of health and wellness. Advanced processes, such as high-moisture extrusion, allow formulators to seamlessly incorporate these functional actives into products without compromising texture or sensory appeal. The rising demand for clean-label products further accelerates this trend, as shoppers actively avoid artificial colors, preservatives, and other synthetic additives. Additionally, the FDA's updated criteria for the "healthy" claim, set to take effect in February 2028, will enforce stricter nutritional standards, creating opportunities for companies that proactively reformulate their offerings to meet these guidelines[2]Source: Food and Drug Administration,"FDA Finalizes Updated “Healthy” Nutrient Content Claim", www.fda.gov . Companies that source bioactive ingredients directly from growers not only enhance their credibility among health-conscious consumers but also mitigate supply chain risks, particularly in this premium-priced and highly competitive segment.

Expansion of snackification as meal replacements

Gen Z and Millennials are shifting away from the traditional three-meal cadence, opting instead for multiple mini-eating moments. This shift reflects changing lifestyles and preferences for more flexible eating patterns. In response, brands are enhancing their offerings with bulkier portions, layered textures, and globally inspired seasonings, aiming to balance indulgence with nutrient density. These innovations cater to consumers seeking convenient yet satisfying options that can replace full meals. A prime example of this trend is the surge in meat snacks, which have outpaced baseline growth due to their protein content meeting satiety demands. Additionally, the inherent portability and long shelf life of meat snacks make them an attractive choice for on-the-go consumption. Furthermore, product developers are scrutinizing amino-acid profiles and glycemic impacts, ensuring these "snack meals" align with specific dietary plans like keto or high-protein regimens. This meticulous approach highlights the industry's commitment to addressing diverse consumer needs while maintaining nutritional integrity.

Growing penetration of e-commerce and quick-commerce

As online shopping surges, retailers are prioritizing thumbnail photography, product ratings, and enhancing last-mile delivery to meet evolving consumer expectations. This shift reflects the growing importance of digital merchandising strategies in capturing consumer attention and driving online sales. To combat temperature fluctuations during transit, companies are increasingly adopting sturdier secondary packaging and incorporating desiccant inserts to maintain the quality of snacks, particularly crisp ones. These measures ensure product integrity and customer satisfaction, even under challenging transportation conditions. Urban dark-store operators, which focus on providing rapid deliveries in densely populated areas, are playing a significant role in reshaping the supply chain. These operators enable faster delivery times but impose higher slotting fees, which are pushing brands to concentrate on promoting high-margin SKUs to offset costs and maintain profitability. Research further highlights that consumers are willing to pay a premium for ultrafast delivery services, particularly for indulgent treats and better-for-you products, reflecting a growing demand for convenience, premium experiences, and health-conscious options.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented unorganized retail and distribution gaps | –0.6% | Asia-Pacific and Africa | Medium term (2–4 years) |

| Volatility in agricultural commodity prices | –0.5% | Global with higher pressure on cost-sensitive segments | Short term (≤ 2 years) |

| Rising scrutiny of HFSS advertising to children | –0.4% | Europe and North America | Long term (≥ 4 years) |

| Tightening single-use-plastic and EPR rules | –0.3% | Led by Europe with global ripple effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented unorganized retail and distribution gaps

In many emerging markets, informal mom-and-pop outlets hold sway, curbing the reach of chilled chains and dampening the potential for premiumization. These outlets dominate due to their accessibility, affordability, and deep-rooted presence in local communities, making it challenging for organized retail formats to penetrate. Additionally, deficits in rural roads and cold storage infrastructure further hinder the distribution and availability of higher-value perishable snacks, limiting their market growth and reducing opportunities for category expansion. While digital B2B ordering apps are making strides in Indonesia, India, and the Philippines, bridging small stores with organized distributors and mitigating stock-out risks, adoption rates vary significantly[3]Source: United States Department of Agriculture,"Snack Foods Market Brief", apps.fas.usda.gov. Factors such as digital literacy, internet connectivity, trust in technology, and the willingness of small retailers to shift from traditional procurement methods to digital platforms contribute to the uneven adoption of these solutions.

Volatility in agricultural commodity prices

Erratic movements in the markets for corn, wheat, and edible oils are being driven by extreme weather events and geopolitical uncertainties. These factors have disrupted supply chains, leading to unpredictable price fluctuations that challenge market stability. Manufacturers without advanced hedging programs or diversified supplier bases are feeling the pinch from these input price swings, as they struggle to absorb the rising costs. In contrast, leading brands are taking proactive measures by securing forward contracts to lock in prices and investing in regenerative sourcing practices to ensure long-term sustainability and reduced risk. These strategies not only help stabilize their operations but also enhance their resilience against future disruptions. However, smaller players, lacking the resources to implement such measures, are grappling with slimmer margins, tighter cash flows, and increased financial vulnerability in this volatile environment. This disparity highlights the growing divide between established market leaders and emerging entrants, as the latter face significant challenges in navigating the current market dynamics.

Segment Analysis

By Product Type: Meat Snacks Drive Premium Growth

In 2024, savory snacks continued to dominate the global snack foods market, commanding a 32.87% share. This stronghold underscores the persistent consumer affinity for salty, crispy treats like potato chips, corn snacks, and pretzels. While competition from healthier snack alternatives is on the rise, savory snacks remain a cherished indulgence across various age groups and regions. Innovations, such as extruded vegetable crisps and pulse-based puffs, are infusing plant-based nutrition into the savory realm. Yet, mainstream consumers still gravitate towards authentic flavors, enticing seasoning blends, and that coveted crunch. Even with the ascent of healthier options, the segment's wide sensory allure cements savory snacks as a go-to for both spontaneous and planned grocery buys.

Meat snacks are carving out a niche as the snack foods market's fastest-growing segment, with projections indicating a robust CAGR of 6.26%. Items like meat sticks and jerky are particularly favored by active, health-conscious consumers, thanks to their portability and high protein content, all without the need for refrigeration. In response to clean-label demands, brands are rolling out product extensions featuring grass-fed beef, turkey, and bison, emphasizing both taste and ethical sourcing. Such innovations resonate especially with premium snack buyers who value flavor and ingredient transparency. The segment is riding the wave of broader protein wellness trends and a pivot away from high-carb snacks. With its dynamic growth, diverse protein offerings, and alignment with modern lifestyles and clean eating, the meat snacks category is steadily increasing its footprint in the global snack foods arena.

Note: Segment shares of all individual segments available upon report purchase

By Ingredient Type: Clean-Label Momentum Accelerates

In 2024, conventional snack food formulas dominated the market, accounting for 63.54% of total revenue. Their stronghold is largely due to cost competitiveness, appealing to mass-market consumers, and the widespread availability of core raw materials. This ensures predictable manufacturing and distribution for producers, leading to steady supply chains and consistent pricing. Additionally, conventional snacks enjoy consumer familiarity, established brand loyalty, and economies of scale that keep costs low. Despite facing stiff competition from health-focused alternatives, their accessibility in both developed and emerging markets solidifies their substantial market share. The segment's pervasive retail presence poses challenges for newer formats, even as niche categories gain traction.

Organic and clean-label snack formulas are on track to achieve a 5.35% CAGR over the forecast period, positioning them as the market's fastest-growing segment. This surge is driven by consumers' readiness to pay a premium for transparency in farming and for formulations that are additive-free and non-GMO. Yet, scaling this segment introduces complexities: processors need to secure certified organic acreage, verify ingredient origins, and uphold stringent traceability. While a projected dip in organic soybean and corn prices may alleviate some cost pressures, brands must navigate procurement judiciously to ensure a steady supply. Companies that spotlight collaborations with farmers and emphasize regenerative agriculture practices stand a better chance of winning over eco-conscious consumers. With shoppers increasingly prioritizing sustainability and health in their choices, organic and clean-label snacks are steadily expanding their footprint in the snack food market.

By Packaging Type: Sustainability Drives Innovation

In 2024, bags and pouches captured 42.17% of the global snack packaging volume, highlighting their market dominance. Their lightweight, portable, and resealable nature caters to diverse consumption occasions. This format's versatile sizing, cost efficiency, and branding flexibility make it a top choice for manufacturers and consumers alike. Technological advancements in packaging are boosting their allure. Leading converters are rolling out mono-material polyolefin films, simplifying recycling without compromising on oxygen or moisture barriers. Major brands, like Mars, are fine-tuning logistics to support this format, evidenced by their adoption of right-size cases, which cut down corrugated-board tonnage, costs, and carbon emissions. Given the rising sustainability expectations and ongoing functional enhancements, bags and pouches are poised to retain their leading position in snack food packaging.

While cans have long been a staple in snack packaging, they're now on track to grow at a 4.63% CAGR, emerging as the category's fastest-growing segment. This revival is primarily due to their recyclability, aligning seamlessly with Extended Producer Responsibility (EPR) mandates and established waste-collection systems in many developed regions. Cans not only safeguard products but also extend shelf life, appealing to manufacturers and consumers who prioritize premium or durable snacks. Their alignment with circular economy principles makes them a top pick for brands emphasizing sustainability. Innovations like lightweight metal alloys and easy-open ends are boosting their market allure. As the global demand for eco-friendly packaging surges, cans are re-establishing their significance and steadily increasing their footprint in snack food packaging.

By Distribution Channel: Digital Transformation Accelerates

In 2024, supermarkets and hypermarkets captured 34.68% of the total snack food expenditure, solidifying their status as the dominant distribution channel. Their prowess stems from presenting a vast array of products, accommodating diverse consumer tastes in one visit. Promotional strategies, including bundle offers, in-store discounts, and loyalty incentives, drive higher-value purchases. These retailers enjoy robust brand collaborations and heightened in-store visibility, fueling impulse buys in the snack segment. The expansive retail format allows shoppers the ease of a one-stop shop, blending essential groceries with tempting snack choices. With a well-established framework, frequent promotional activities, and the ability to showcase both emerging and established brands, supermarkets and hypermarkets continue to be pivotal in global snack distribution.

Online retail is poised to expand at a CAGR of 5.64%, emerging as the quickest-growing channel for snack distribution. This surge is fueled by increasing smartphone adoption, making app-driven grocery shopping more reachable. Swift delivery services enable near-instant snack access, merging convenience with variety. Subscription snack boxes introduce a novel discovery facet, letting consumers sample global tastes and niche brands from their homes. Furthermore, this platform empowers brands with targeted promotions, tailored suggestions, and direct consumer interaction. With the digital landscape broadening and logistics fortifying, online retail's foothold in the snack market is set to intensify, posing a challenge to traditional brick-and-mortar establishments in the coming years.

Geography Analysis

In 2024, the Asia-Pacific region claimed the largest share of global revenue at 31.68%, driven by urbanization, rising middle-class incomes, and a deep-rooted cultural preference for savory and spicy flavors. China, with its retail snack sales surpassing 1 trillion yuan, owes much of its success to domestic champions adept at fusing traditional ingredients with contemporary processing methods. Meanwhile, regional research and development centers are swiftly introducing localized products, like seaweed-infused chips in Japan and chili-mango gummies in Thailand.

The Middle East and Africa is set to experience the fastest growth, projected at a 4.83% CAGR through 2030. This surge is fueled by youthful demographics, a rise in e-commerce, and a rebound in tourism. Both Saudi Arabia and the United Arab Emirates are channeling significant investments into food processing hubs and logistics networks, aiming to lessen import dependencies and harness re-export opportunities. Seasonal peaks in spending are driven by premium gifting assortments during Ramadan and Diwali, alongside a growing trend towards functional snacks, mirroring global wellness trends.

North America, Europe, and South America navigate a landscape of mature market penetration, each with its distinct regulatory and economic nuances. The U.S. market, while a stronghold for high-protein and artisanal products, grapples with commodity-price fluctuations that challenge price sensitivity. Europe takes the lead in stringent policies, especially concerning plastics and HFSS marketing, pushing brands towards constant reformulation and innovative packaging designs. In South America, Brazil and Mexico stand out as growth powerhouses, even as they contend with currency volatility and a fragmented retail landscape that complicates nationwide expansions. Across all continents, businesses are increasingly recognizing the necessity of integrated risk-management strategies, addressing sourcing challenges, climate resilience, and multi-modal freight solutions.

Competitive Landscape

In the global snack foods arena, power dynamics play out between established multinationals and nimble disruptors, resulting in a moderately concentrated market. Giants like PepsiCo, Mondelez, Nestlé, and the recently merged Mars-Kellanova entity boast diverse portfolios, harnessing global reach for efficient procurement and advertising. A case in point: PepsiCo’s robotics-driven plants showcase the potential of manufacturing digitization to minimize downtime and cut indirect costs.

Merger and Acquisition strategies dominate as key players seek to bridge portfolio gaps. In February 2025, Mars bolstered its portfolio by integrating Kellanova’s savory assets, gaining ground in Pringles and Cheez-It, and fortifying its stance against salty-snack competitors. Meanwhile, Flowers Foods acquired Simple Mills to enhance its clean-label image, and UpSnack Brands brought Pipcorn and Spudsy into the fold, pushing the envelope on upcycled innovation. Emerging brands are leveraging direct-to-consumer strategies and social media narratives to clinch shelf space, particularly in the realms of functional protein bites and gut-health products.

Sustainability in packaging has emerged as a pivotal focus. Amcor, in collaboration with select brand partners, introduced recycle-ready laminates that align with retailer standards. Simultaneously, Kind Snacks tested curbside-recyclable paper wraps, achieving an impressive 93% shopper purchase intent. By outsourcing to specialized co-packers like Tandem Foods, brand owners can redirect funds from fixed plant assets to research and development and consumer engagement.

Snack Food Industry Leaders

-

General Mills Inc.

-

PepsiCo Inc.

-

Kellogg Company

-

Nestle SA

-

Mondelez International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- August 2025: Pop Secret unveiled its new ready-to-eat popcorn, now offered in 5-ounce packages featuring Homestyle Sea Salt, Double Cheddar, and Movie Theater Butter flavors. This launch aims to cater to the growing demand for convenient and flavorful snacking options among consumers.

- August 2025: Lays introduced a limited-edition flavor: Hot Chilli Squid Potato Chips. This unique flavor addition reflects the brand's strategy to experiment with bold and innovative tastes to attract adventurous snack enthusiasts.

- June 2025: Bee Up debuted a honey-based snack lineup, crafted with real honey and devoid of synthetic dyes, flavors, and preservatives. These treats come in Sour Watermelon, Very Berry, and Tropical Mix flavors, targeting health-conscious consumers seeking natural and wholesome snack alternatives.

- January 2025: Rice Chippies rolled out a new rice-based snack, proudly presented in 100% recyclable packaging. This initiative aligns with the brand's commitment to sustainability while offering consumers an eco-friendly snacking choice.

Global Snack Food Market Report Scope

A snack is a small portion of food eaten between meals. Snacks come in various forms and shapes, including packaged snack foods and other processed foods.

The snack food market is segmented by type, distribution channel, and geography. Based on type, the market is segmented into frozen snacks, savory snacks, fruit snacks, confectionery snacks, bakery snacks, and other types. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Product Type | Frozen Snacks | |

| Savoury Snacks | ||

| Fruit Snacks | ||

| Confectionery Snacks | ||

| Bakery Snacks | ||

| Meat Snacks | ||

| Others | ||

| By Ingredient Type | Conventional | |

| Organic/Clean-Label | ||

| By Packaging Type | Bags/Pouches | |

| Cans | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

By Product Type

| Frozen Snacks |

| Savoury Snacks |

| Fruit Snacks |

| Confectionery Snacks |

| Bakery Snacks |

| Meat Snacks |

| Others |

By Ingredient Type

| Conventional |

| Organic/Clean-Label |

By Packaging Type

| Bags/Pouches |

| Cans |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the snack foods market in 2025?

The snack foods market size reached USD 280.24 billion in 2025.

What is the expected growth rate through 2030?

The sector is forecast to log a 4.23% CAGR over 2025–2030.

Which region generates the most snack sales?

Asia-Pacific held the largest share at 31.68% of 2024 global revenue.

Which product type is growing the fastest?

Meat snacks are projected to expand at a 6.26% CAGR to 2030.

How are sustainability regulations affecting packaging?

Extended-producer-responsibility rules are accelerating the shift toward recycle-ready films and higher recycled-content formats.

Page last updated on: