Dementia Drugs Market Size and Share

Market Overview

| Study Period | 2021 - 2030 |

|---|---|

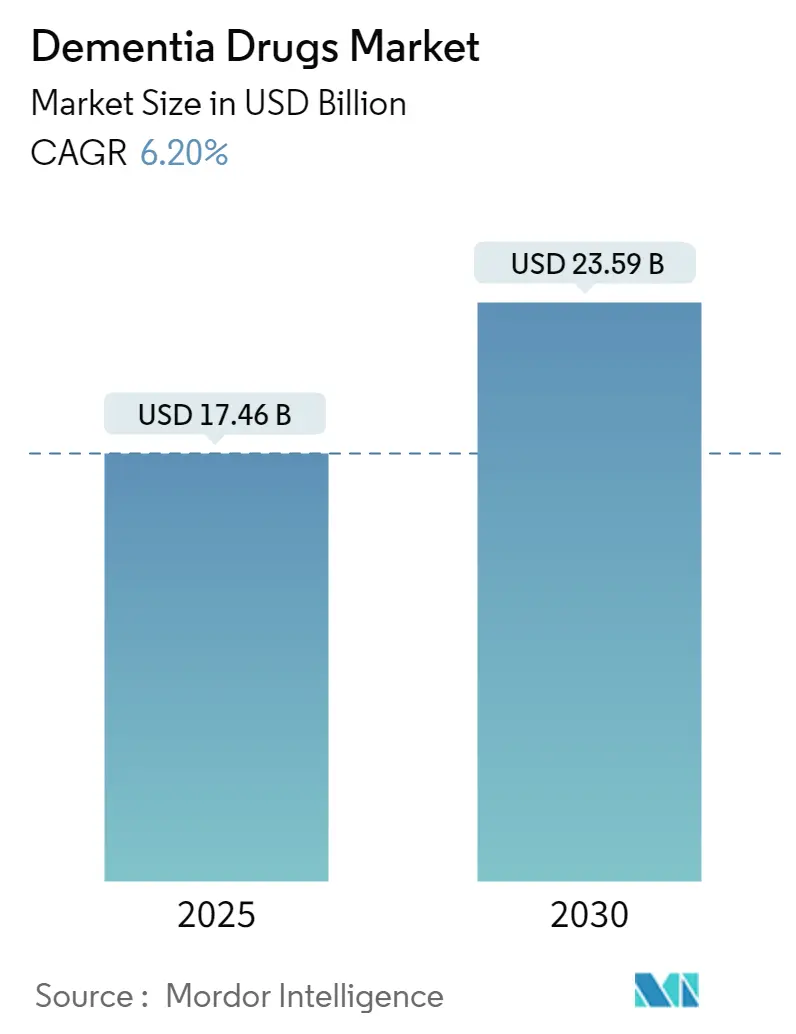

| Market Size (2025) | USD 17.46 Billion |

| Market Size (2030) | USD 23.59 Billion |

| Growth Rate (2025 - 2030) | 6.20% CAGR |

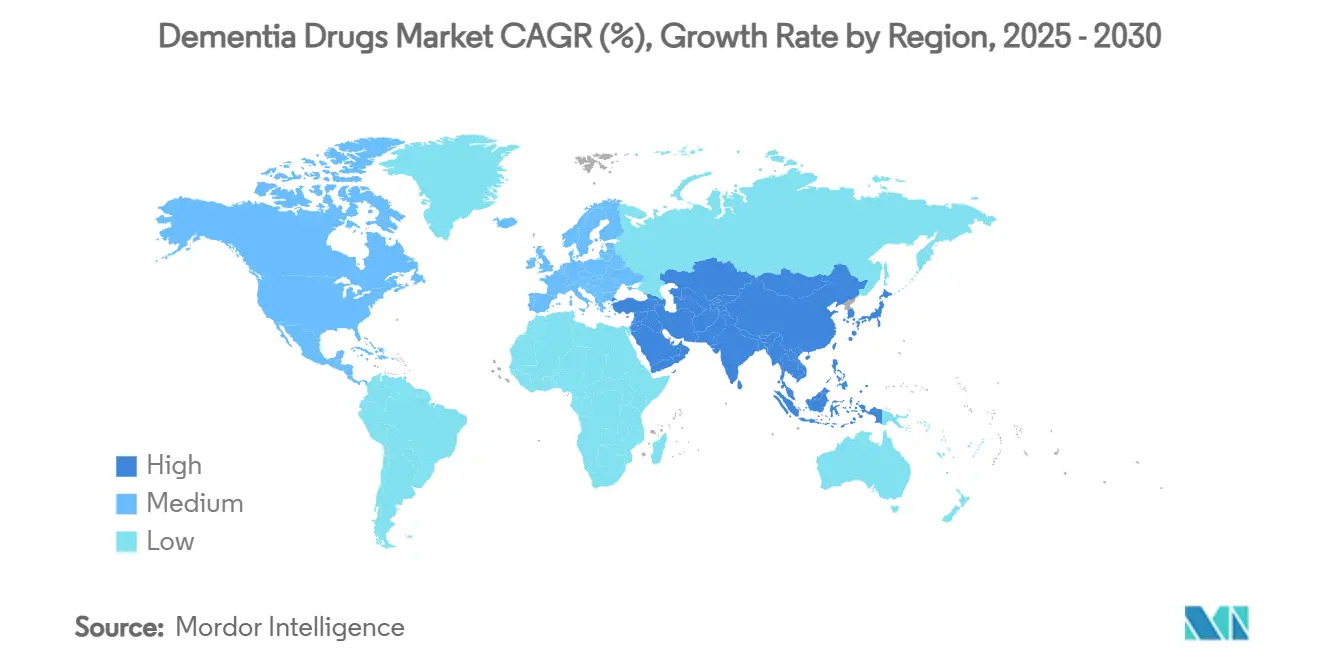

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dementia Drugs Market Analysis by Mordor Intelligence

The dementia therapeutics market size stands at USD 17.46 billion in 2025 and is forecast to reach USD 23.59 billion by 2030, reflecting a 6.20% CAGR over the period. Strong demand for disease-modifying anti-amyloid antibodies, widening diagnostic uptake, and supportive national dementia strategies underpin the expansion, even as reimbursement bodies apply tighter value thresholds. Competitive intensity is rising as incumbents safeguard first-mover advantages while smaller biotechnology firms explore tau, neuroinflammation, and gene-based targets. Digital cognitive assessment aids and AI-enabled discovery platforms accelerate patient identification and pipeline velocity, deepening the addressable population. At the same time, manufacturing complexity for biologics and ARIA-related adherence challenges temper the near-term trajectory of the dementia therapeutics market.

Key Reports Takeaways

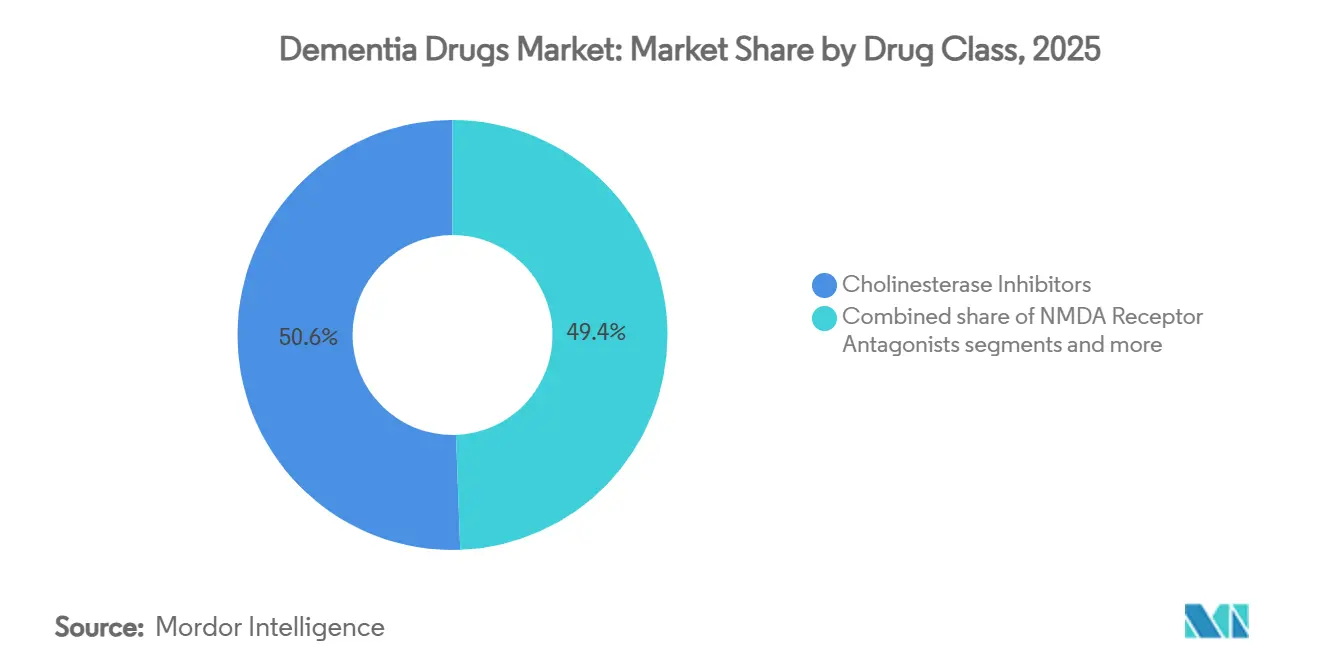

- Cholinesterase inhibitors captured 50.57% of dementia therapeutics market share in 2024, whereas anti-amyloid monoclonal antibodies are projected to expand at a 6.92% CAGR through 2030.

- Alzheimer’s disease accounted for 61.15% of the dementia therapeutics market size in 2024 and mild cognitive impairment is set to grow at a 7.10% CAGR to 2030.

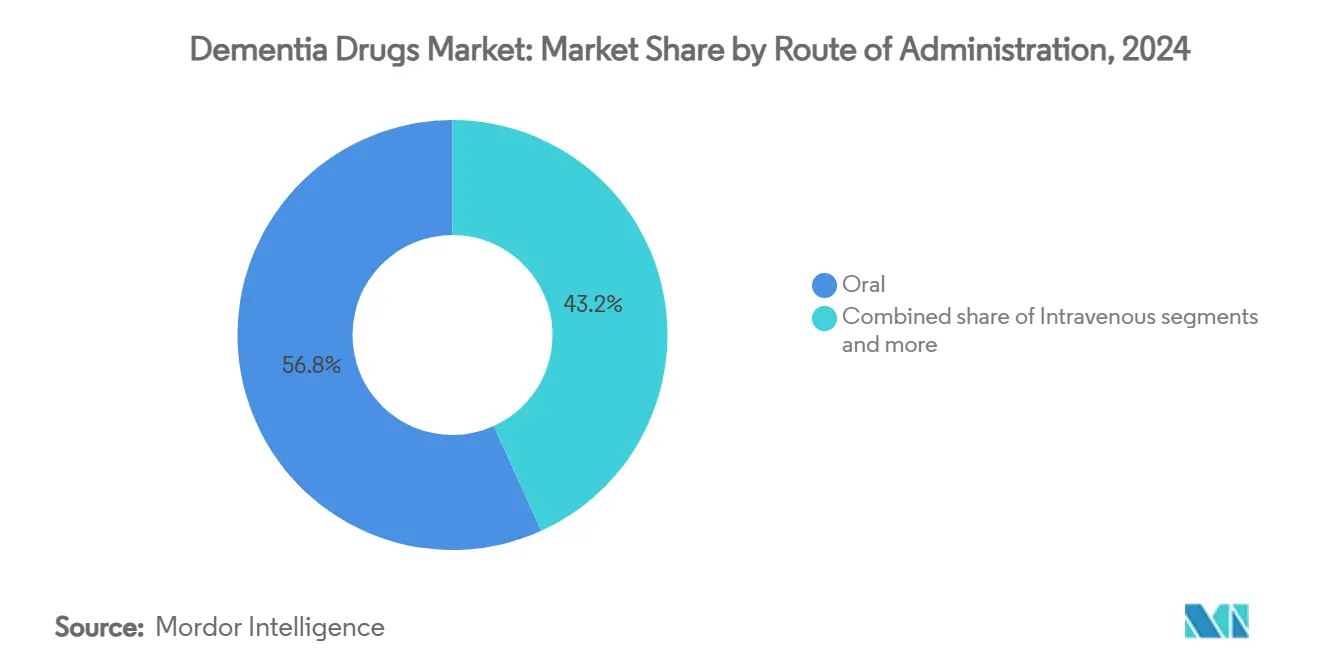

- Oral products led with 56.77% of revenue in 2024, but intravenous infusions hold the highest projected CAGR at 7.29% through 2030.

- Hospital pharmacies commanded 54.60% of 2024 sales and are advancing at a market-leading 7.48% CAGR.

Global Dementia Drugs Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & dementia prevalence surge | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Approvals of disease-modifying anti-amyloid therapies | +0.8% | North America & Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of diagnostic biomarkers & PET tracers | +0.6% | North America & Europe, selective Asia-Pacific markets | Medium term (2-4 years) |

| Digital therapeutics & combination regimens emerging | +0.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Government dementia plans & funding momentum | +0.3% | North America, Europe, Australia, selective Asia-Pacific | Long term (≥ 4 years) |

| AI-enabled drug-discovery platforms shorten R&D cycles | +0.2% | Global, concentrated in major pharma hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Dementia Prevalence Surge

Rapid population ageing is swelling the dementia therapeutics market as the 65-plus cohort expands faster than any other age group. Dementia incidence doubles roughly every five years after 65, and the World Health Organization projects global cases will triple by 2050. Japan, South Korea, Italy, and Germany exhibit the most acute near-term prevalence spikes, whereas India, Brazil, and Indonesia will encounter steeper late-decade surges in absolute patient numbers. Governments that view dementia as a socioeconomic threat are allocating larger budgets to early diagnosis, caregiver support, and research infrastructure. Insurers increasingly reimburse biomarker-guided interventions, enlarging the treated pool and reinforcing prescription growth. Collectively these dynamics anchor a structurally long-run expansion path for the dementia therapeutics market.

Approvals of Disease-Modifying Anti-Amyloid Therapies

The 2024 FDA nod for Eli Lilly’s Kisunla and the 2025 European authorization of Eisai’s Leqembi verify the amyloid hypothesis after decades of setbacks[1]Source: Eisai Co. Ltd., “Leqembi Three-Year Data Presented at AAIC 2024,” eisai.com . These milestones convert pent-up demand for disease-modifying options into realized sales and catalyze development of infusion centers, diagnostic PET capacity, and monitoring pathways. Conditional approvals in certain jurisdictions create tiered pricing but also stimulate value-based contracts that reward real-world cognitive preservation. Three-year Leqembi data demonstrating sustained benefits further strengthens physician confidence. Collectively, these factors inject momentum into the dementia therapeutics market and spur pipeline diversification into amyloid-plus-tau combination regimens.

Growing Adoption of Diagnostic Biomarkers & PET Tracers

Mandatory amyloid confirmation before anti-amyloid initiation has driven a sharp rise in PET scan volumes and CSF biomarker usage. The FDA’s 2024 clarification of computerized cognitive assessment pathways unlocked market access for tools such as CognICA and Cognivue Clarity[2]Source: Nature Publishing Group, “Validation of Cognivue Clarity for Mild Cognitive Impairment,” nature.com, widening community-based screening beyond memory clinics. Earlier detection enlarges the mild cognitive impairment cohort eligible for disease-modifying drugs, accelerating uptake. Regional reimbursement remains uneven, yet U.S. Medicare coverage of new tracer codes signals an inflection point likely to be emulated by Japan and Germany. As diagnostic costs decline, biomarker algorithms are being embedded into AI-powered decision support, further extending the reach of the dementia therapeutics market.

Digital Therapeutics & Combination Regimens Emerging

Regulators now recognize digital cognitive training programs like NeuroNation MED as Class II medical devices, enabling their prescription alongside pharmacotherapy. Continuous monitoring generates patient-specific data that optimize dosing intervals and flag ARIA-related symptoms early. Pharmaceutical companies are pairing apps with infusions to satisfy payers’ demand for measurable functional outcomes, creating bundled reimbursement codes that boost adherence. Combination regimens, for example anti-amyloid plus anti-tau antibodies, have entered Phase 2 with preliminary signals of additive efficacy. These shifts are redefining competitive positioning inside the dementia therapeutics market and sowing the seeds for holistic care platforms rather than standalone pills.

Restraint Imoact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High clinical-trial failure rates & investment risk | -0.9% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Stringent HTA / reimbursement hurdles | -0.7% | Europe core, expanding to Asia-Pacific & emerging markets | Medium term (2-4 years) |

| Limited patient adherence owing to adverse events | -0.5% | Global, with regional variations in monitoring capabilities | Short term (≤ 2 years) |

| Supply-chain dependence on complex biologic manufacturing | -0.3% | Global, with concentration risks in specialized facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Clinical-Trial Failure Rates & Investment Risk

Historic Alzheimer’s attrition exceeds 90%, eclipsing oncology and cardiovascular benchmarks. Failures in 2024 by Roche, Sage, and Otsuka reaffirm investor caution, elevating hurdle rates and slowing private funding. Neurological endpoints, placebo effects, and heterogeneous patient biology complicate statistical powering, pushing costs beyond USD 1 billion per Phase 3 program. While adaptive trial designs and digital biomarkers promise efficiencies, the risk–reward calculus still curtails capital inflows and restrains the dementia therapeutics market from achieving faster growth.

Stringent HTA / Reimbursement Hurdles

NICE’s 2024 draft refusals for Leqembi and Kisunla on cost-effectiveness grounds underscore Europe’s tough pricing climate. Health technology bodies often omit caregiver burden and indirect societal costs from QALY models, undervaluing long-term disease-modifying benefits. Germany’s AMNOG process and Japan’s cost-utility thresholds echo similar constraints. Without robust real-world evidence, list-price concessions or risk-sharing schemes, widespread European uptake may lag North America and blunt part of the dementia therapeutics market potential.

Segment Analysis

By Drug Class: Anti-Amyloid Therapies Challenge Traditional Dominance

Cholinesterase inhibitors maintained a commanding 50.57% share of the dementia therapeutics market in 2024, affirming their role as front-line management for mild to moderate Alzheimer’s disease. Nonetheless, anti-amyloid monoclonal antibodies recorded the category’s fastest expansion, supported by a 6.92% CAGR outlook and fresh approvals across North America, Europe, and South Korea. NMDA receptor antagonists continue to address moderate-to-severe stages but face limited differentiation. Pipelines centred on anti-tau and kinase inhibitors have gained FDA Fast Track tags, broadening commercial optionality. Production scalability and infusion infrastructure remain the primary gating factors for monoclonal antibody prescriptions, yet sustained cognitive benefit data are converting neurologists and solidifying reimbursement support, thereby deepening anti-amyloid penetration within the dementia therapeutics market.

Looking ahead, competitive dynamics hinge on portfolio breadth and manufacturing agility. Johnson & Johnson’s posdinemab received Fast Track status in January 2025, prompting rivals to accelerate combination trials pairing amyloid and tau mechanisms. Bristol Myers Squibb’s repurposing of Cobenfy signals a broader move toward multi-indication platforms that straddle psychosis, agitation, and cognition. Amid these shifts, the dementia therapeutics market size for anti-amyloid drugs is forecast to double by 2030, whereas legacy categories plateau, forcing incumbents to diversify or risk share erosion.

Note: Segment shares of all individual segments available upon report purchase

By Indication: MCI Emerges as High-Growth Opportunity

Alzheimer’s disease retained a formidable 61.15% share of the dementia therapeutics market in 2024, bolstered by symptomatic and disease-modifying options. Yet mild cognitive impairment has surfaced as the fastest-growing niche, tracking a 7.10% CAGR through 2030 as biomarker-guided diagnosis expands in primary care. Cognivue Clarity and CognICA screenings differentiate MCI from normal ageing with high specificity, opening an earlier therapeutic window[2]. Parkinson’s disease dementia and Lewy-body conditions maintain meaningful, though smaller, treatment footprints; Ambroxol and other repositioned agents in Phase 3 could lift penetration by late decade.

Early-stage intervention raises pivotal questions on treatment length, payer budgets, and patient selection. U.S. Medicare’s draft coverage restricts anti-amyloid infusion to biomarker-confirmed MCI or mild dementia, underscoring the linkage between diagnostics and revenue growth. In Asia-Pacific, national reimbursement is contingent on local cost-utility files, but ageing populations in Japan and South Korea will swell absolute candidate pools.

By Route of Administration: IV Infusions Gain Momentum

Oral delivery continued to dominate with 56.77% of 2024 sales, valued for convenience and lower monitoring needs. However, intravenous formulations, principally anti-amyloid antibodies, are charting a 7.29% CAGR, the fastest across modalities, signalling a significant shift in the dementia therapeutics market. Hospitals and specialist infusion centres are scaling capacity, often supported by manufacturer-funded MRI programs aimed at ARIA surveillance. Transdermal patches offer niche benefits for dysphagic patients and caregivers seeking simplified regimens, yet development portfolios remain thin.

Product selection is increasingly route-dependent: payers lean toward IV infusions where disease modification has been clinically demonstrated, while primary care physicians favour oral generics for symptomatic relief. Cold-chain and chair-time costs weigh on facility budgets, driving experimentation with subcutaneous variants that may debut after 2027. Should these formulations match IV efficacy, they could recapture patients deterred by infusion logistics, rebalancing modality shares within the dementia therapeutics market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Hospital Pharmacies Dominate Growth

Hospital pharmacies generated 54.60% of total revenue in 2024 and are expected to outpace all other channels at a 7.48% CAGR through 2030. Complex preparation protocols, infusion supervision, and reimbursement paperwork centralise biologic dispensing in acute care settings, reinforcing the operational dominance of hospitals in the dementia therapeutics market. Retail outlets continue to supply oral cholinesterase inhibitors and NMDA antagonists, but their share erodes as prescribers shift toward disease-modifying infusions.

Online pharmacies remain embryonic, restricted mainly to maintenance scripts and constrained by cold-chain challenges. Nonetheless, direct-to-patient delivery models are piloting home-based subcutaneous administration, which could eventually migrate some volume away from hospitals. Pharmacies embedded within integrated health systems possess an edge in data sharing and outcomes documentation, elements that payers are integrating into value-based contracts governing the dementia therapeutics market.

Geography Analysis

North America continues to lead the dementia therapeutics market, sustained by favourable reimbursement, early regulatory endorsements, and extensive clinical research infrastructure. Medicare’s national coverage determination for amyloid PET imaging removes a critical barrier, allowing more accurate patient selection and reinforcing payer confidence in cognitive benefit trajectories. Canada’s deliberative approach stresses cost-utility, but provincial pilot programmes are paving access for biomarker-confirmed mild cognitive impairment. Mexico, although smaller, is witnessing the rise of private neurology networks that import U.S.-approved biologics for high-income cohorts, indicating an emergent cross-border niche.

Asia-Pacific’s momentum is grounded in sheer demographic scale alongside rising per-capita healthcare spend. Japan’s super-aged society drives near-term volume, supported by a strong domestic diagnostics industry capable of supplying amyloid and tau tracers. South Korea’s single-payer system has quickly integrated Leqembi under risk-sharing reimbursement, demonstrating institutional readiness to embrace expensive disease-modifying therapies. China remains a wildcard: its large patient pool offers unmatched upside, yet evolving regulatory rules and supply-chain frictions introduce execution risks. India and Indonesia will initially prioritise symptomatic generics, but rising middle-class affordability foreshadows long-run biologic demand that could reshape the dementia therapeutics market.

Europe delivers steady but moderated growth. National HTA bodies continue to constrain list prices, compelling companies to accept confidential discounts or contingent-value agreements. Germany’s rapid adoption of new diagnostics balances slower therapeutic uptake in the UK and Spain. France’s national dementia plan incorporates caregiver stipends, indirectly easing treatment adoption by offsetting ancillary costs. Eastern European markets trail in both diagnostic capacity and reimbursement scope, yet EU structural funds earmarked for geriatric care upgrades may lift baseline infrastructure. Overall, Europe’s policy environment favours gradual rather than explosive contributions to the dementia therapeutics market size.

Competitive Landscape

Industry structure remains moderately concentrated, anchored by Biogen, Eisai, and Eli Lilly, whose first-to-market anti-amyloid franchises confer manufacturing economies and clinician familiarity. Barriers include large-scale bioreactor ownership, validated diagnostic ecosystems, and multi-national regulatory teams capable of navigating diverse HTA regimes. Nevertheless, competition is intensifying as Johnson & Johnson, Roche, and Novartis pursue tau and neuroinflammation assets that could erode incumbent share in the next five years.

Technology alliances constitute a primary competitive lever. Roche’s AI collaboration seeks to stack a pipeline of sub-1-nanomolar potency molecules, while Eisai has partnered with a digital therapeutics firm to package Leqembi alongside cognitive-training software in Japan. Smaller innovators such as Voyager Therapeutics are advancing gene-silencing constructs aimed at halting tau production after a single dose, potentially leapfrogging chronic infusion paradigms. These developments broaden therapeutic diversity and complicate forecasting for the dementia therapeutics market.

Pricing and access strategies are equally decisive. Eli Lilly has initiated outcome-based contracts with U.S. payers tied to MMSE score preservation, whereas Biogen explores flat-rate subscription models for integrated drug-plus-diagnostic bundles. Some manufacturers propose royalty-free licenses in low-income countries to head off parallel importation. As players experiment with differentiated commercial frameworks, market position will hinge not only on scientific merit but also on health-economic storytelling that resonates with payers and policy makers assessing the dementia therapeutics market.

Dementia Drugs Industry Leaders

-

Johnson and Johnson

-

Teva Pharmaceuticals

-

Aurobindo Pharma

-

Zydus Cadila

-

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Johnson & Johnson received FDA Fast Track status for posdinemab, a phosphorylated-tau monoclonal antibody targeting early Alzheimer’s disease

- January 2025: Bristol Myers Squibb positioned Cobenfy for Alzheimer’s-related agitation and cognition with projected peak sales of USD 10 billion

- July 2024: Eli Lilly secured FDA approval for Kisunla (donanemab) in early symptomatic Alzheimer’s disease

Global Dementia Drugs Market Report Scope

Dementia is the loss of cognitive functioning, thinking, remembering, reasoning, and behavioral abilities to such an extent that it interferes with a person's daily life and activities. These functions include memory, language skills, visual perception, problem-solving, self-management, and the ability to focus and pay attention. Alzheimer's is the most common cause of dementia.

The Dementia Drugs Market is Segmented by Indications (Lewy Body Dementia, Parkinson's Disease Dementia, Alzheimer's Disease, Vascular Dementia, and Other Indications), Drug Class (MAO Inhibitors, Glutamate Inhibitors, and Cholinesterase Inhibitors), and Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, and Rest of Middle East and Africa), and South America Brazil, Argentina, and Rest of South America)). The report offers value (in USD million) for the above segments.

| By Drug Class | Cholinesterase Inhibitors | |

| NMDA Receptor Antagonists | ||

| Anti-Amyloid Monoclonal Antibodies | ||

| Multi-target Kinase & Other Emerging Classes | ||

| By Indication | Alzheimer’s Disease | |

| Parkinson’s Disease Dementia | ||

| Lewy-Body & Frontotemporal Dementias | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Transdermal | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| Cholinesterase Inhibitors |

| NMDA Receptor Antagonists |

| Anti-Amyloid Monoclonal Antibodies |

| Multi-target Kinase & Other Emerging Classes |

| Alzheimer’s Disease |

| Parkinson’s Disease Dementia |

| Lewy-Body & Frontotemporal Dementias |

| Oral |

| Intravenous |

| Transdermal |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

1. What is the current value of the dementia therapeutics market?

The dementia therapeutics market size is USD 17.46 billion in 2025 and is projected to reach USD 23.59 billion by 2030.

2. Which drug class is growing fastest?

Anti-amyloid monoclonal antibodies are expanding at a 6.92% CAGR through 2030 as newly approved disease-modifying therapies gain traction.

3. Why is Asia-Pacific the most attractive growth region?

Rapid population ageing, expanding healthcare spending, and favourable reimbursement decisions in Japan and South Korea are propelling a 7.67% CAGR.

4. What barriers limit European uptake?

Stringent health technology assessment criteria, particularly cost-effectiveness thresholds, delay reimbursement for high-priced biologics.

Page last updated on: