Security Robot Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

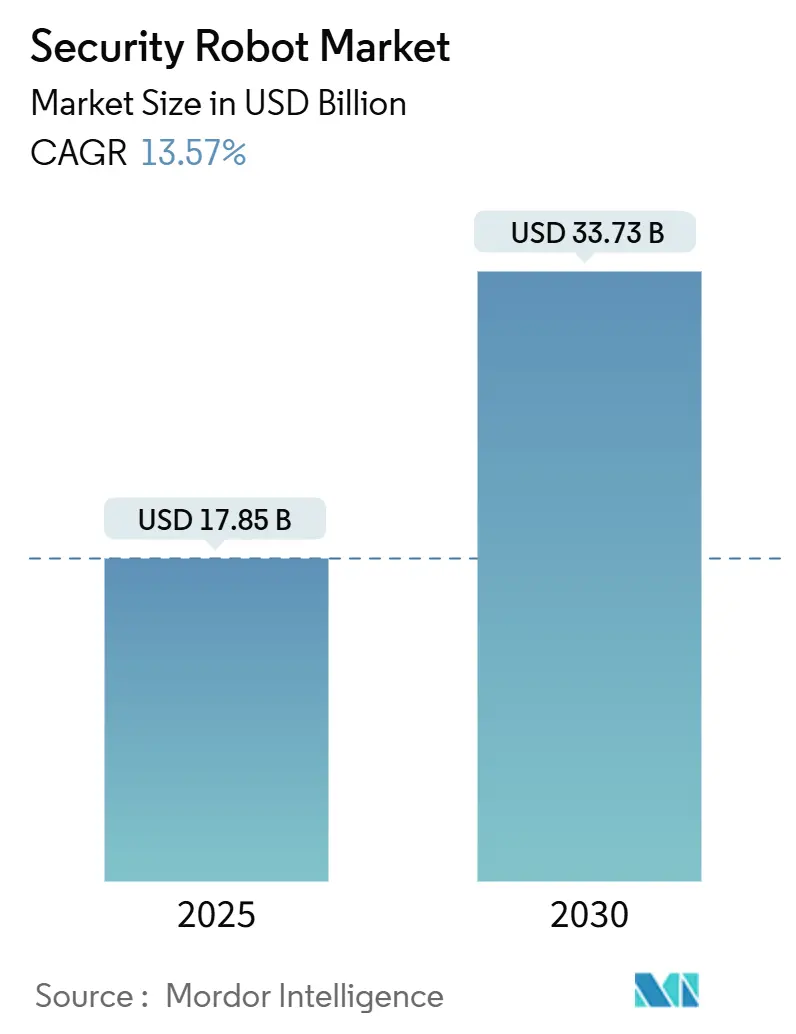

| Market Size (2025) | USD 17.85 Billion |

| Market Size (2030) | USD 33.73 Billion |

| Growth Rate (2025 - 2030) | 13.57% CAGR |

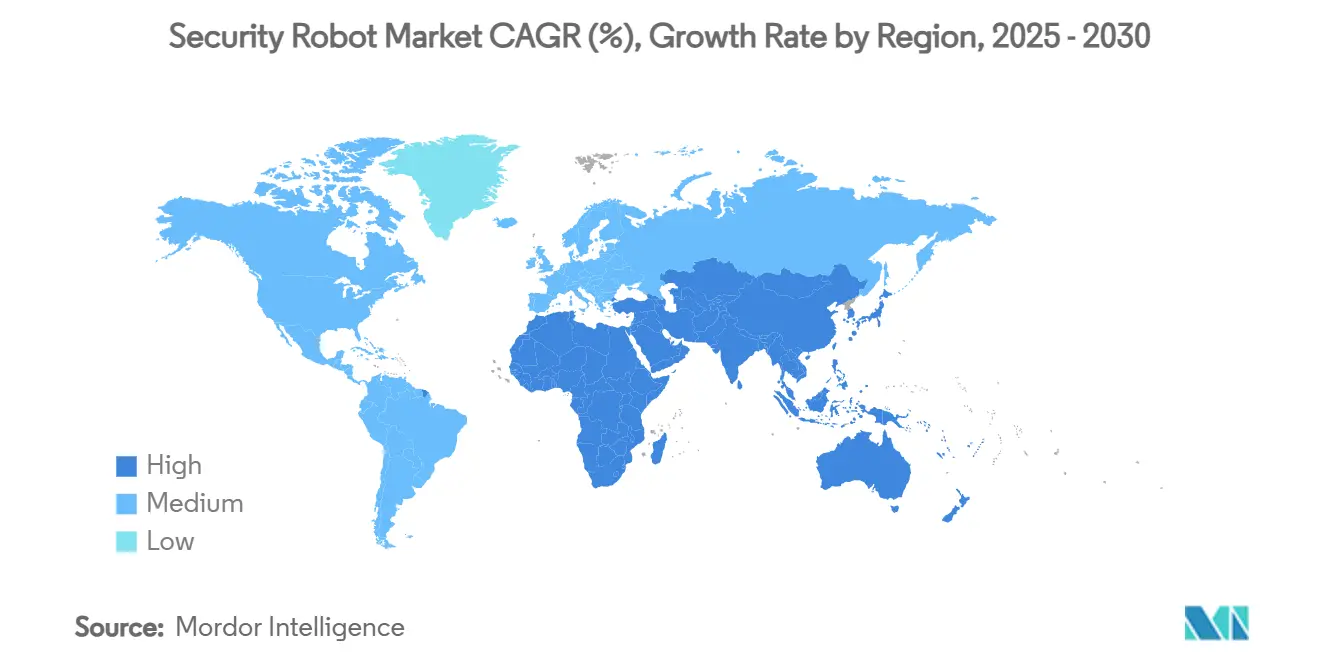

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Security Robot Market Analysis by Mordor Intelligence

The security robotics market reached USD 17.85 billion in 2025 and is forecast to advance to USD 33.73 billion by 2030, reflecting a robust 13.57% CAGR. Demand is rising because autonomous platforms now blend AI perception, advanced sensors, and all-domain navigation into systems that operate continuously and predict threats before they materialize. Defense installations, airports, power plants, and commercial campuses increasingly replace fixed cameras and roving guards with robots that deliver round-the-clock coverage, lower false-alarm rates, and cut personnel expenses. Growth is further reinforced by subscription pricing that removes upfront capex, by national mandates for perimeter intrusion detection at critical infrastructure, and by regulatory progress that opens Beyond Visual Line of Sight (BVLOS) air corridors for drones. Meanwhile, cyber-hardening gaps, fragmented spectrum policy, and public unease over facial recognition create headwinds that vendors must manage through technology design and transparent governance.

Key Report Takeaways

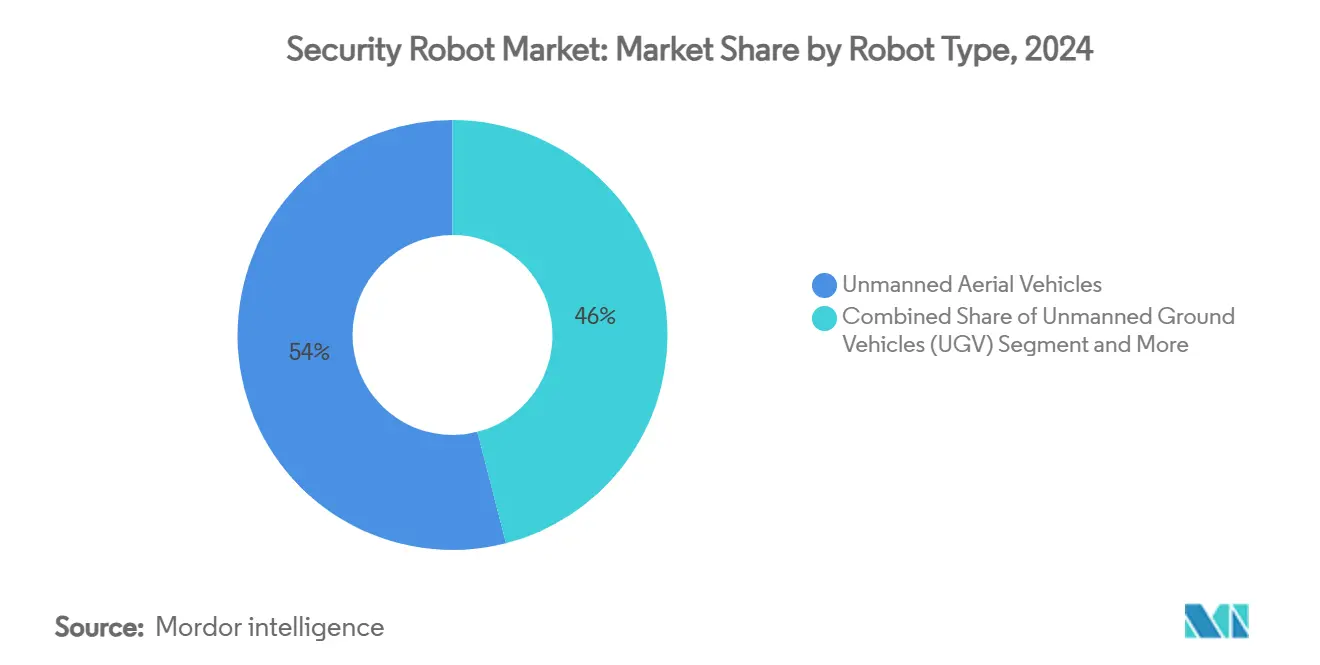

- By robot type, Unmanned Aerial Vehicles (UAVs) led with 54% revenue share in 2024; Unmanned Ground Vehicles (UGVs) are projected to expand at a 15.2% CAGR to 2030.

- By component, hardware captured 68% of the security robotics market share in 2024, while services are advancing at an 18.9% CAGR through 2030.

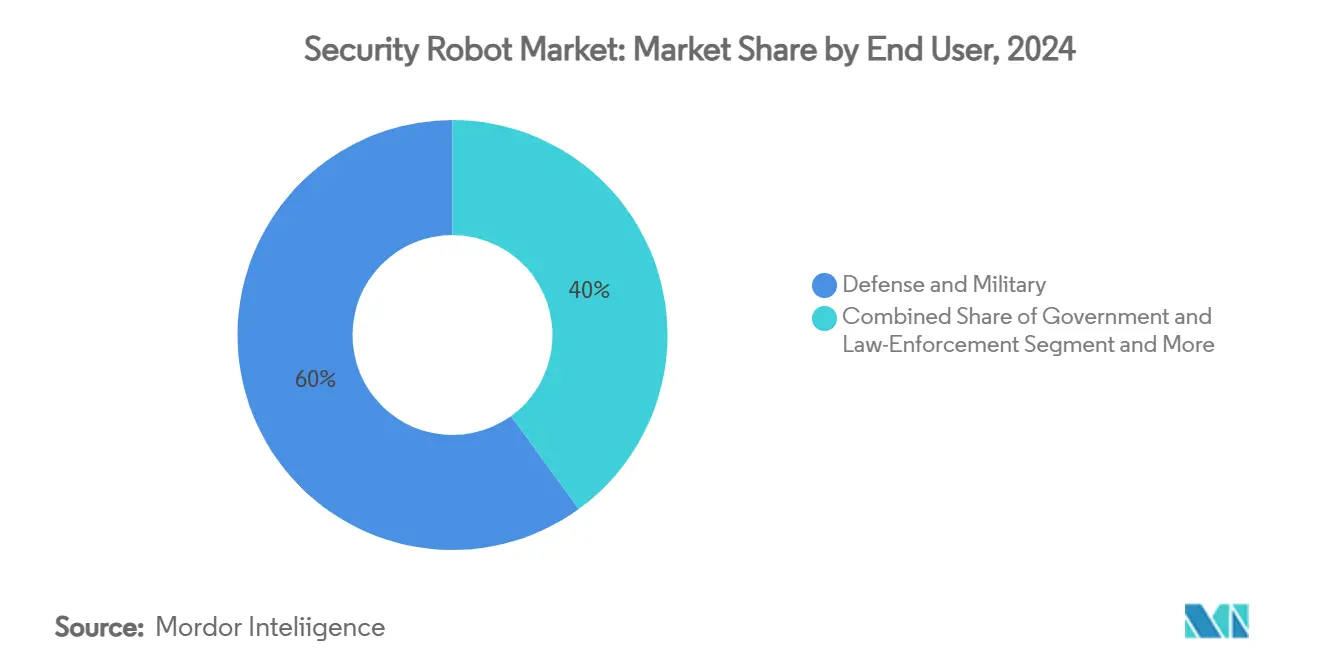

- By end user, defense and military applications held 60% of the security robotics market share in 2024; commercial and industrial facilities record the highest projected CAGR at 17.6% up to 2030.

- By application, patrolling and surveillance accounted for 45% of the security robotics market size in 2024 and explosive detection and disposal is growing at 17% CAGR through 2030.

- By geography, North America commanded 40% of revenue in 2024, whereas Asia-Pacific is forecast to expand at a 15.4% CAGR to 2030.

Global Security Robot Market Trends and Insights

Drivers Impact Analysis

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Deployment of AI-enabled perception stacks lowering false-alarm rates | +2.8% | North America and Europe | Medium term (2–4 years) |

| Expansion of civilian BVLOS drone corridors for security patrols | +2.1% | Asia-Pacific core, spill-over to MEA | Long term (≥4 years) |

| Mandates for perimeter intrusion detection at energy assets | +1.9% | Middle East and North Africa | Short term (≤2 years) |

| Adoption of robot-as-a-service by commercial real-estate operators | +2.3% | North America, expanding to Europe | Medium term (2–4 years) |

| Accelerated demand for indoor UGVs triggered by retail shrink crisis | +1.7% | North America and Europe | Short term (≤2 years) |

| Growing naval budgets for autonomous underwater ISR | +1.6% | Asia-Pacific, Australia, India | Long term (≥4 years) |

Source: Mordor Intelligence

Deployment of AI-enabled perception stacks lowering false-alarm rates

Thermal imaging fused with multi-spectral cameras and computer-vision models has cut nuisance alarms by 40%, easing operator workload at airports and nuclear plants. NVIDIA’s Cosmos platform feeds Vision-Language-Action models that interpret context, letting robots distinguish normal activity from genuine threats. Energy companies that integrated these stacks trimmed incident response times by 50% because operators receive precise coordinates and threat classifications.[1]Energy Robotics, “Autonomous Security Robots for Critical Infrastructure,” energy-robotics.com Superior detection accuracy shifts robots from experimental trials to mission-critical roles.

Expansion of civilian BVLOS drone corridors for security patrols in Asia

Australia and Japan now permit BVLOS patrols through risk-based regulatory frameworks that keep drones beyond pilot sight while maintaining safety via detect-and-avoid systems. Single aircraft can secure multi-kilometer perimeters that previously demanded dozens of guards, amplifying coverage and lowering cost per hectare. Governments across the Indo-Pacific see autonomous patrols as essential for vast coastlines and remote installations, spurring regional demand.

Mandates for perimeter intrusion detection at energy assets in the Middle East

Saudi Arabia’s Public Investment Fund earmarked USD 100 billion for robotics under its Alat initiative, making autonomous monitoring mandatory at oil and gas sites after a series of perimeter breaches.[2]Diplomatic Courier, “Saudi Arabia’s Expanding Role in Advanced Technologies,” diplomaticourier.com Rugged robots equipped with thermal sensors detect intruders across harsh desert terrain where humans struggle. Formal performance benchmarks accelerate procurement and standardize technical requirements for vendors.

Adoption of robot-as-a-service by commercial real-estate operators in the USA

Subscription pricing lets property owners access robots at roughly USD 11 per hour versus USD 35–85 for guards, delivering up to 65% cost savings. Providers bundle maintenance and software upgrades, removing technical hurdles. Data analytics from patrol logs help reduce insurance premiums and improve tenant satisfaction, driving widespread uptake.

Restraints Impact Analysis

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented radio-frequency spectrum regulations limiting multi-robot fleets | -1.8% | European Union, expanding globally | Medium term (2–4 years) |

| Public backlash against face-recognition patrol bots in municipal deployments | -1.2% | Europe, North America urban areas | Short term (≤2 years) |

| High total cost of ruggedised all-terrain platforms for petro-chemical sites | -0.9% | Middle East, harsh environment regions | Long term (≥4 years) |

| Cyber-hardening gaps exposing C2 links to spoofing and jamming | -2.1% | Global, particularly contested environments | Short term (≤2 years) |

Source: Mordor Intelligence

Fragmented radio-frequency spectrum regulations limiting multi-robot fleets

EU member states allocate spectrum differently, forcing vendors to customize radios for each country and undermining economies of scale. The 2024 EU AI Act also classifies security robots as high-risk systems, piling on compliance paperwork that inflates costs.[3]European Parliament, “Regulation (EU) 2024/1689 on Artificial Intelligence,” eur-lex.europa.eu These hurdles discourage small providers and delay multi-nation deployments, especially at cross-border facilities.

Cyber-hardening gaps exposing command-and-control links to spoofing and jamming

Researchers uncovered backdoors in imported quadruped robots, enabling unauthorized takeover. GPS spoofing can mislead unmanned vehicles, while jammers disrupt C2 channels during critical incidents. Because cyber-physical security frameworks remain less mature than traditional IT controls, operators hesitate to rely solely on robots for perimeter defense.

Segment Analysis

By Robot Type: UAVs Dominate While UGVs Accelerate

UAVs retained 54% of the security robotics market in 2024 thanks to rapid deployment and wide-area coverage that slash response times during perimeter breaches. Platforms integrate electro-optical, infrared, and acoustic sensors to track intruders day and night. The security robotics market size attributed to UAV patrols is projected to expand steadily through 2030 as BVLOS rules mature. Indian and Australian navies also push demand for extra-large autonomous underwater vehicles (XLUUVs) that extend surveillance into contested littorals.

UGVs represent the fastest-growing segment with a 15.2% CAGR because indoor malls, warehouses, and data centers need persistent ground-level monitoring where aerial flight is impractical. Retailers grappling with theft adopt compact UGVs that stream real-time video to control rooms and issue audible deterrence announcements. When linked via 5G, multiple robots coordinate patrols, creating a mesh that reduces blind spots. Vendors enhance autonomy with lidar-based SLAM and cloud-hosted AI, tightening loops between detection, classification, and response actions. Hybrid amphibious robots and AUVs carve a specialized niche around ports and offshore platforms, addressing threats that cross land–sea boundaries.

Note: Segment shares of all individual segments available upon report purchase

By Component: Hardware Dominance Shifts Toward Service Innovation

Hardware captured 68% of 2024 revenue because perception sensors, compute modules, and rugged chassis still carry high production costs. Lidar units, thermal cameras, and edge GPUs account for most of the bill of materials, anchoring near-term sales. Yet services are racing ahead at 18.9% CAGR as end users pivot to operating-expenditure models. RaaS bundles deliver robots, software, and field support under multi-year contracts, freeing customers from depreciation concerns. In 2024 Knightscope demonstrated that upgrading its entire K5 fleet to the v5 configuration incurred zero incremental cost to clients, underscoring the value proposition of subscription offerings.

Software and AI stacks generate sticky revenue through annual licenses that unlock advanced analytics, natural-language interfaces, and integration APIs. Over time, these digital layers command higher margins than hardware. Cloud dashboards let security directors monitor dispersed robot fleets, run forensics on incident video, and push over-the-air algorithm updates, creating a virtuous circle that ties users to a vendor’s ecosystem and expands the total addressable security robotics market.

By End User: Defense Investment Meets Commercial Disruption

Defense and military sites absorbed 60% of 2024 spending, underpinned by multi-year government programs for force protection and intelligence collection. The U.S. Department of Defense’s DARPA contracts fund AI tools that improve coordinated missions among airborne assets. Naval agencies procure sea-floor crawlers and underwater gliders to track submarines and mines, broadening the security robotics market relevance across domains.

Commercial and industrial facilities, however, post the fastest 17.6% CAGR. Labor shortages and rising guard wages push factories, logistics hubs, and office parks to deploy robots that work 24/7 without overtime. Robots capture structured data—such as badge tailgating events—that feeds predictive analytics for loss prevention. Insurance carriers increasingly offer premium discounts when autonomous patrols lower incident frequency, helping justify investment.

Note: Segment shares of all individual segments available upon report purchase

By Application: Surveillance Still Leads but Specialized Missions Rise

Patrolling and surveillance delivered 45% of 2024 revenue and remain the anchor for deployments because continuous situational awareness underpins every other mission. Robots circle campuses, scan access points, and stream alerts to security operation centers that integrate with PSIM platforms. The security robotics market size allocated to patrol tasks will keep growing steadily, although share declines as specialized missions scale.

Explosive detection and disposal grows fastest at 17% CAGR, propelled by airports, stadiums, and transit hubs that confront heightened threat levels. Robots fitted with chemical sensors and robotic arms investigate suspicious packages from a standoff distance, protecting staff and the public. Meanwhile, search-and-rescue and hazardous-materials response robots work inside fires, gas leaks, and collapse zones, extending the technology’s humanitarian profile beyond pure security.

Geography Analysis

North America generated 40% of 2024 revenue, supported by unrivaled defense budgets, early BVLOS legislation, and venture funding for robotics start-ups. The United States alone fields 1,200-plus autonomous patrol units across malls, corporate campuses, and municipal parking structures. Knightscope deployments cut incidents by up to 50% within months, convincing mid-tier cities to pilot fleets as a force multiplier. Canada and Mexico adopt similar solutions for border crossings and energy corridors, reinforcing regional scale advantages.

Asia-Pacific posts the highest 15.4% CAGR thanks to regulatory overtures that permit long-range drone patrols and surging naval budgets. Australia’s USD 140 million Ghost Shark XLUUV program exemplifies undersea robotics investment, while China showcases humanoid police robots that interact with citizens on the streets of Shenzhen. India’s navy plans 12 indigenous XLUUVs for anti-submarine warfare, confirming pent-up demand for maritime domain awareness in contested waters.

Europe advances steadily but contends with complex AI and spectrum regulations that stretch project timelines. High-profile defense initiatives such as Thales’s £1.8 billion maritime sensor contract and QinetiQ’s £160 million directed-energy program sustain momentum. Still, spectrum fragmentation hampers seamless multi-robot coordination across borders, compelling integrators to tailor communications systems country by country.

Competitive Landscape

The market remains moderately fragmented. Traditional defense primes—Lockheed Martin, Northrop Grumman, Thales—retain an edge in classified missions and high-end platforms. They reinforce capabilities through acquisitions, illustrated by AeroVironment’s USD 4.1 billion purchase of BlueHalo, which broadened its portfolio across air, land, sea, space, and cyber domains.

Specialist vendors drive commercial adoption with subscription models. Knightscope, Cobalt AI, and SMP Robotics supply malls, hospitals, and warehouses where clients favor operating-expense contracts over capital purchases. Boston Dynamics teams with ASSA ABLOY to link quadrupeds to secure door locks, forging end-to-end intrusion response workflows.

Technology differentiation centers on perception software. Providers race to reduce false positives, extend autonomy into GNSS-denied zones, and harden communications against spoofing. Those with mature AI stacks can license algorithms across multiple robot form factors, diversifying revenue. Partnerships between security service majors and robotics manufacturers accelerate market penetration; Allied Universal has integrated more than 17,000 guards with autonomous platforms under its Enhanced Protection Services banner.

Security Robot Industry Leaders

-

Lockheed Martin Corporation

-

Northrop Grumman Corporation

-

Thales SA

-

Knightscope Inc.

-

SZ DJI Technology Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Israel Ministry of Defense awarded Elbit Systems USD 40 million for HuntAIR-X drone swarm management and THOR mini-UAS.

- June 2024: QinetiQ secured a £160 million UK MoD extension for DragonFire laser and RF directed-energy weapons.

- May 2025: AeroVironment closed its USD 4.1 billion acquisition of BlueHalo, adding cyber and directed-energy segments.

- May 2025: Australian-built SG-1 Fathom underwater gliders processed acoustic data 40 times faster than analysts, impressing the Royal Australian Navy.

Global Security Robot Market Report Scope

Security robots are designed to replace patrolling security guards and to provide mobile CCTV monitoring. A security robot automatically moves around a restricted area without direct operator supervision. Images from its built-in cameras are transmitted to the security station.

The security robots market is segmented by type of robot (unmanned aerial vehicle, unmanned ground vehicle, and autonomous underwater vehicle), end user (defense and military, residential, and commercial), application (spying, explosive detection, patrolling, rescue operations, and other applications), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the market sizes and forecasts for all the above segments in value (USD).

| By Type | Unmanned Ground Vehicles (UGV) | ||

| Autonomous Underwater Vehicles (AUV) | |||

| Hybrid/Amphibious Robots | |||

| By Component | Hardware | ||

| Software and AI Stack | |||

| Services (Integration, RaaS, MRO) | |||

| By End User | Defense and Military | ||

| Government and Law-Enforcement | |||

| Commercial and Industrial Facilities | |||

| Residential and Private Estates | |||

| By Application | Patrolling and Surveillance | ||

| Explosive Detection and Disposal | |||

| Spying and Reconnaissance | |||

| Search and Rescue / Disaster Response | |||

| Fire and Hazardous-Environment Response | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East | Israel | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Unmanned Ground Vehicles (UGV) |

| Autonomous Underwater Vehicles (AUV) |

| Hybrid/Amphibious Robots |

| Hardware |

| Software and AI Stack |

| Services (Integration, RaaS, MRO) |

| Defense and Military |

| Government and Law-Enforcement |

| Commercial and Industrial Facilities |

| Residential and Private Estates |

| Patrolling and Surveillance |

| Explosive Detection and Disposal |

| Spying and Reconnaissance |

| Search and Rescue / Disaster Response |

| Fire and Hazardous-Environment Response |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the security robotics market?

The security robotics market is valued at USD 17.85 billion in 2025 and is projected to reach USD 33.73 billion by 2030.

Which robot type holds the largest share today?

Unmanned Aerial Vehicles account for 54% of 2024 revenue because they deliver rapid, wide-area surveillance.

Why are services growing faster than hardware?

Robot-as-a-service bundles avoid capital expenditure, provide software updates, and cut hourly costs to roughly one-third of human guard rates, driving an 18.9% CAGR.

Which region is expanding the quickest?

Asia-Pacific leads with a 15.4% CAGR as governments approve BVLOS drone corridors and invest in autonomous underwater surveillance.

What is the main restraint facing multi-robot deployments in Europe?

Fragmented spectrum regulation and the EU AI Act impose distinct compliance steps in each country, delaying cross-border fleet rollouts.

How do robots improve cost efficiency for commercial real estate?

Subscription-priced patrol units cost about USD 11 per hour, delivering up to 65% savings and reducing incidents by as much as 50% within months of deployment.

Page last updated on: July 6, 2025