Cannabis Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

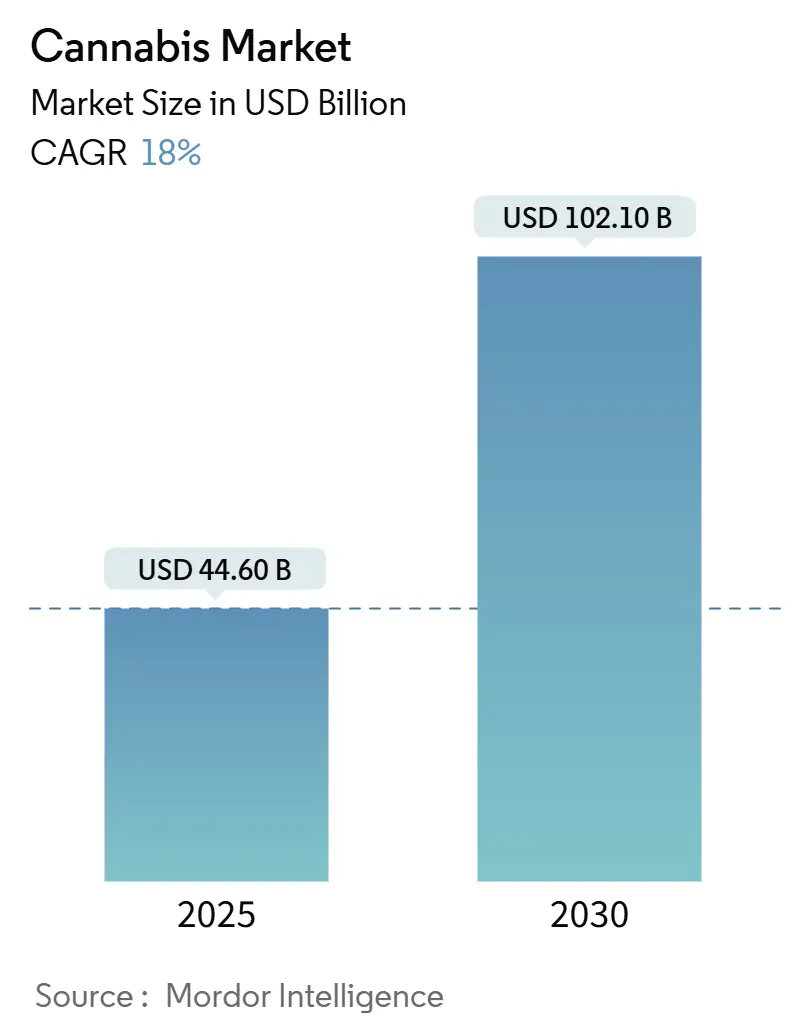

| Market Size (2025) | USD 44.60 Billion |

| Market Size (2030) | USD 102.10 Billion |

| Growth Rate (2025 - 2030) | 18.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cannabis Market Analysis by Mordor Intelligence

The cannabis market reached USD 44.6 billion in 2025 and is projected to grow to USD 102.1 billion by 2030, at a CAGR of 18.0% during the forecast period. This growth is driven by potential federal rescheduling in the United States, increased adult-use legalization in Europe, and expanding medical cannabis programs across Asia-Pacific. Investment from consumer packaged goods, beverage, and pharmaceutical companies is accelerating product development, while advanced cultivation technologies improve production efficiency and reduce costs for integrated operators. The oversupply in established North American markets is causing price compression and industry consolidation. Environmental concerns regarding indoor cultivation facilities have led to investments in sustainable operations and efficient climate control systems, which reduce operational costs and enhance market positioning.

Key Report Takeaways

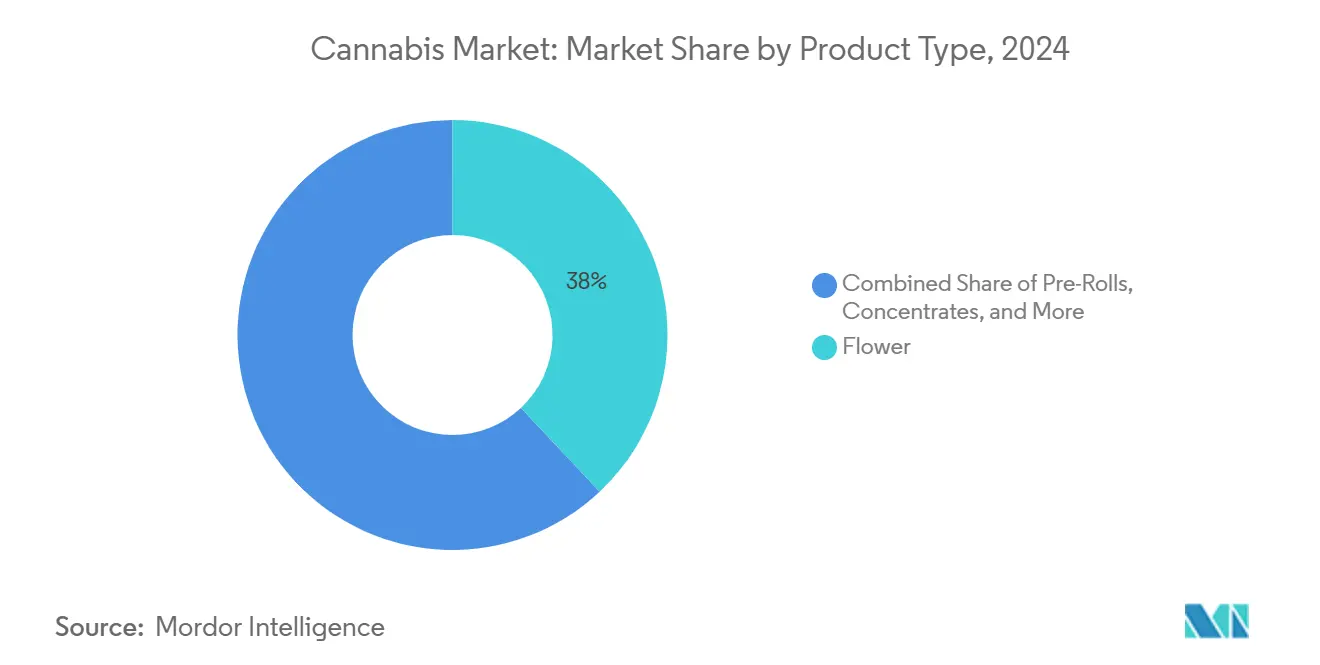

- By product type, flowers dominated with a 38% revenue share in 2024, while beverages are projected to grow at the highest CAGR of 20.6% during 2025-2030.

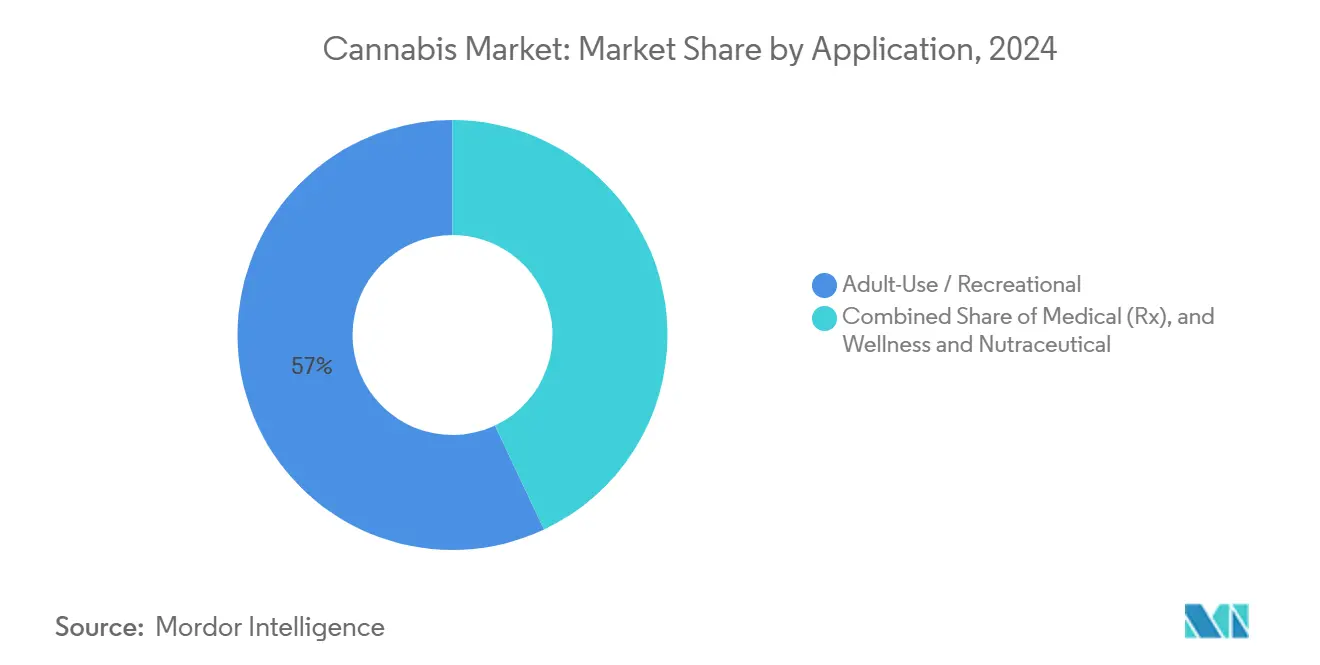

- By application, the adult-use segment/recreational held 57% of the cannabis market share in 2024, with wellness and nutraceutical applications projected to grow at a 22.2% CAGR through 2030.

- By compound type, THC-dominant products captured 58% of the cannabis market size in 2024, while minor cannabinoids are anticipated to register a 23.1% CAGR.

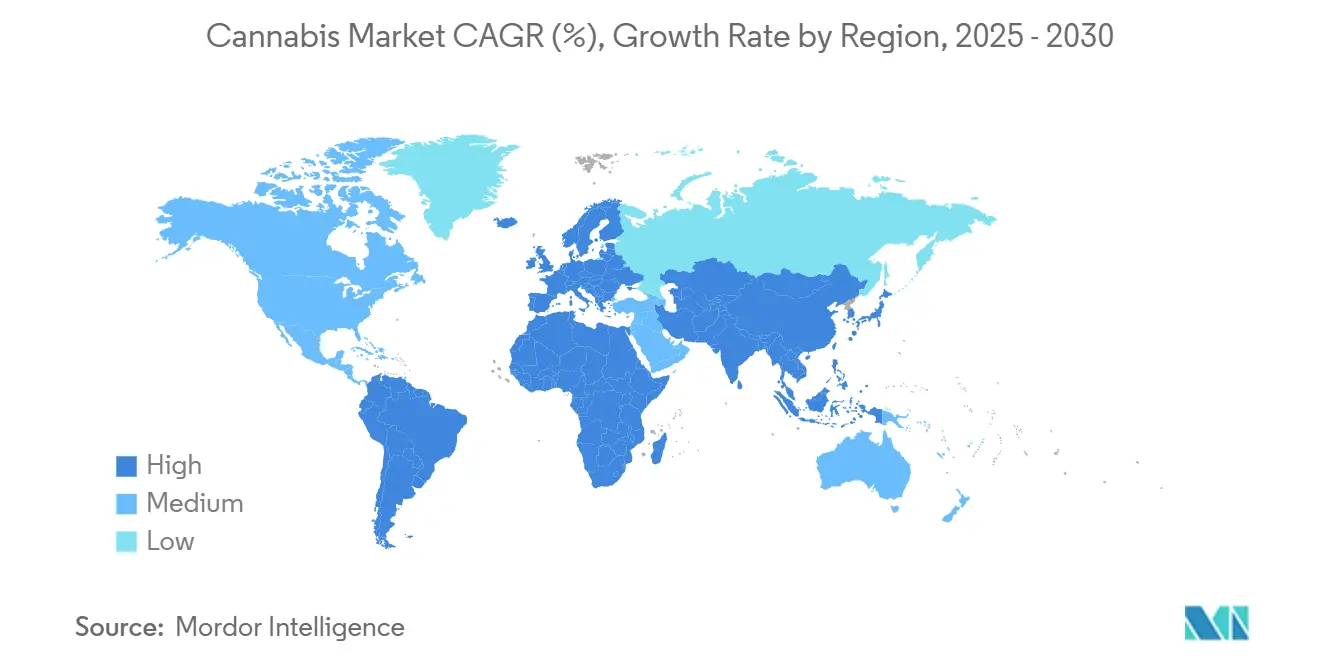

- By geography, North America generated 65% of the revenue in 2024, while Asia-Pacific is projected to witness the fastest growth at a 20.1% CAGR through 2030.

Global Cannabis Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wave of adult-use legalization and Schedule-III rescheduling momentum | +4.2% | North America, spillover to Europe and Asia-Pacific | Medium term (2-4 years) |

| Expansion of national reimbursement for cannabis-based medicines | +3.1% | Global, with early gains in Germany, Canada, Australia | Long term (≥ 4 years) |

| Rising demand for cannabidiol wellness and functional products | +2.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Strategic cross-industry investments from CPG/pharmaceutical/alcohol majors | +2.4% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Commercialization of pharmaceutical-grade minor cannabinoids | +3.5% | Global, with Research and Development hubs in North America and Europe | Long term (≥ 4 years) |

| AI-enabled precision cultivation improving yields and margins | +1.8% | Global, early adoption in North America | Short term (≤ 2 years) |

Source: Mordor Intelligence

Wave of Adult-Use Legalization and Schedule-III Rescheduling Momentum

The proposed federal rescheduling of cannabis in the United States has prompted 12 additional jurisdictions to prepare reform bills for 2025. The potential removal of Section 280E taxes would reduce effective tax rates from their current level of over 70%, improving cash flow for licensed operators.[1]U.S. Department of Justice, “DEA Moves to Reschedule Cannabis,” justice.gov Germany's Cannabis Act implementation in April 2024 establishes the country as Europe's largest regulated market and provides a regulatory framework for neighboring countries. Thailand's commitment to decriminalization continues to influence adoption across the Asia-Pacific region, particularly in medical tourism. Improved regulatory clarity reduces lending risk, enabling mainstream banks to participate and allowing multi-state operators to expand using lower-cost debt financing. The expansion of legal access increases the eligible consumer base and enhances long-term revenue prospects for companies serving both recreational and medical markets.

Expansion of National Reimbursement for Cannabis-Based Medicines

Public health insurance in Canada, Germany, and Australia now covers specific cannabidiol and THC formulations, reducing patient expenses for chronic care treatments. Jazz Pharmaceuticals' Epidiolex achieved sales of USD 845.5 million in 2023, with projections indicating USD 972 million in 2024, demonstrating the market potential for prescription cannabinoids. Germany's reclassification of cannabis from the Narcotics Act reduces administrative burden, resulting in annual cost savings of USD 2.29 million (EUR 2 million) for healthcare providers and insurance companies. Phase III clinical trials in pain management, oncology, and neurology continue to strengthen the scientific evidence base, encouraging public health systems to expand their formularies. The standardization of clinical protocols facilitates international trade of pharmaceutical-grade cannabis extracts, with Canada, Colombia, and Portugal emerging as key exporters.

Rising Demand for Cannabidiol Wellness and Functional Products

Hemp-derived CBD products, including beverages, gummies, and topicals, meet the demands of health-conscious consumers who are reducing alcohol consumption and seeking plant-based alternatives. Research indicates that 50% of Generation Z adults moderate their alcohol intake, which beverage companies interpret as a long-term consumer behavior change. Major retailers now stock CBD products in beauty and sports nutrition sections, increasing product visibility and mainstream acceptance. Online direct-to-consumer sales channels complement physical retail stores, enabling companies to collect consumer data and optimize product formulations. Anticipated FDA guidelines on hemp ingredients will address labeling requirements, potentially expanding the market for functional foods, including protein bars and ready-to-drink teas.

Strategic Cross-Industry Investments from CPG, Pharmaceutical, and Alcohol Majors

Major consumer goods companies, including Philip Morris International, Brown-Forman, and Constellation Brands, have included cannabis-related risk factors in their SEC filings, indicating their market monitoring activities.[2]U.S. Securities and Exchange Commission, “Brown-Forman 2024 Form 10-K,” sec.gov Investment strategies span from minority positions in edibles companies to complete acquisitions of beverage manufacturers. Companies are utilizing existing distribution networks through partnerships to enable faster national product launches. The pharmaceutical industry provides expertise in clinical studies, stability testing, and GMP compliance, which enhances quality standards across the cannabis industry. Companies that develop products with established brands and secure prime retail placement gain significant competitive advantages.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited banking and capital access due to federal conflicts | -2.9% | North America, spillover globally | Medium term (2-4 years) |

| Inconsistent global dosing and quality standards | -1.8% | Global, hampers international trade | Long term (≥ 4 years) |

| Chronic oversupply driving price compression in mature markets | -3.4% | North America, expanding to Europe | Short term (≤ 2 years) |

| High energy intensity and carbon footprint of indoor cultivation | -1.6% | Global, regulatory pressure in Europe and California | Medium term (2-4 years) |

Source: Mordor Intelligence

Limited Banking and Capital Access Due to Federal Conflicts

Less than 1.5% of New York banks and credit unions provide services to licensed cannabis operators, compelling these businesses to maintain large cash reserves and pay employees in physical currency. Financial institutions face high compliance costs due to suspicious activity reporting requirements, deterring them from entering the cannabis market. The absence of credit card processing prevents e-commerce subscription services, reducing accessibility for medical patients requiring ongoing treatments. International mergers and acquisitions face challenges as buyers cannot utilize federally insured banks for fund transfers. Despite Schedule III rescheduling, cannabis's status as a controlled substance creates uncertainty regarding eligibility for Small Business Administration loans.

Chronic Oversupply Driving Price Compression in Mature Markets

Oregon's wholesale flower prices reached record lows as inventories grew to nearly double the annual demand. Massachusetts experienced a 62% decline in retail prices between 2018 and 2024, eliminating profit margins for small dispensaries.[3]U.S. Securities and Exchange Commission, “Brown-Forman 2024 Form 10-K,” sec.gov Michigan's cannabis industry recorded its first employment decline as retail prices decreased 56% from January 2022 levels. California faces USD 730 million in unpaid excise taxes from closed cultivation operations. The market oversupply reduces new investments, increases bankruptcies, and forces distressed asset sales, altering the competitive landscape.

Segment Analysis

By Product Type – Beverages Drive Innovation Beyond Traditional Flower

Flower remains the primary revenue driver, accounting for 38% of 2024 revenue, due to established cultivation expertise and consumer familiarity. While the segment benefits from diverse genetics and low entry barriers, oversupply conditions create downward pricing pressure. Beverages are projected to grow at a CAGR of 20.6% during 2025-2030. Major beverage companies, including Constellation Brands and Diageo Ventures, are developing infused sparkling waters, tonics, and elixirs that align with traditional social consumption patterns. Advancements in shelf-stable emulsions and rapid-onset nanoemulsions have resolved previous challenges in dosing consistency and taste, improving consumer accessibility.

Vertically integrated operators reduce exposure to flower price fluctuations by expanding into edibles, concentrates, and topicals. Pre-rolls maintain market share through convenience appeal, while vapes attract experienced consumers seeking high potency and mobility. Edibles gain market acceptance through standardized packaging and laboratory testing that complies with European and Canadian import regulations. The introduction of pet products, nasal sprays, and fast-dissolving films demonstrates the market's expansion into diverse consumer applications. The maturing industry creates opportunities for logistics providers through beverage co-packing and cold-chain distribution services, extending economic benefits beyond cultivation and retail operations.

Note: Segment shares of all individual segments available upon report purchase

By Application – Wellness Segment Challenges Adult-Use Dominance

Adult-use cannabis accounted for 57% of 2024 sales, driven by successful state ballot initiatives and social acceptance campaigns. The integration of cannabis into music festivals, sports sponsorships, and lifestyle marketing has helped normalize recreational consumption. The wellness and nutraceutical segment demonstrates the highest growth rate at 22.2% CAGR, supported by aging demographics and increasing focus on preventive healthcare. CBD products, particularly in functional foods and topical applications, attract consumers seeking non-psychoactive solutions for anxiety, inflammation, and sleep issues. The medical legitimacy of CBD products is strengthening as insurance providers in Germany and Australia begin covering pharmacist-dispensed formulations, creating overlap between wellness and medical channels.

The medical cannabis segment remains significant, especially in regions without adult-use legislation. Patient enrollment is increasing in Spain, Israel, and Brazil through expanded qualifying conditions, enhanced telemedicine access, and improved physician education programs. Wellness products maintain higher price points as consumers accept increased costs for quality-verified and specifically formulated products. The nutraceutical segment benefits from growing disposable income levels in Asia-Pacific urban regions. While recreational cannabis faces pricing pressure from market oversupply, wellness product diversification provides cultivators and brands with an opportunity to maintain profit margins in the cannabis market.

Note: Segment shares of all individual segments available upon report purchase

By Compound Type – Minor Cannabinoids Emerge as Premium Category

THC-dominant products maintain market leadership with a 58% share in 2024, driven by adult-use consumer preference for psychoactive effects. Products with balanced THC:CBD ratios serve users seeking moderate effects, while CBD-dominant products address daytime use and pediatric treatment needs. Minor cannabinoids, including CBG, CBN, and THCV, demonstrate the highest growth rate at 23.1% CAGR, with each compound targeting specific therapeutic applications such as appetite control and neuroprotection. The development of biosynthetic production methods enables pharmaceutical-grade materials for clinical trials and patent applications, supporting prescription market growth.

International manufacturers now offer products with specified cannabinoid ratios to demonstrate combined therapeutic effects and increase consumer understanding of wellness benefits. The higher production costs and limited scale of rare cannabinoids support premium pricing strategies. Regulatory changes in European and Australian markets permit pharmacists to create customized cannabinoid formulations for specific medical conditions. Companies that maintain verified Certificates of Analysis for their products gain market advantages as import regulations become more stringent. Organizations developing intellectual property in yeast-based biosynthesis establish revenue streams through licensing as the market shifts toward targeted therapeutic applications.

Geography Analysis

North America generated 65% of 2024 revenue, driven by state programs and potential federal rescheduling that may eliminate 280E tax obligations. U.S. multistate operators expand operations as 12 states prepare adult-use ballots in 2025, while Canadian producers benefit from export opportunities to Germany and Israel. However, mature states face margin pressure from oversupply and compliance costs. The industry continues to face banking restrictions, increasing security expenses, and limiting growth. Mexico awaits Supreme Court guidance on adult-use legislation, though implementation challenges remain.

Europe grows following Germany's Cannabis Act implementation, which increased registered patients from 250,000 in April 2024 to nearly 900,000 by May 2025. Imports supply half of German demand, benefiting Canadian and Portuguese cultivators. The Czech Republic, Luxembourg, and Croatia evaluate adult-use frameworks based on German results. The European Medicines Agency initiates harmonization discussions to address dosing inconsistencies affecting cross-border trade. The United Kingdom emphasizes clinical trials and sustainable production, exemplified by Glass Pharms' anaerobic digestion-powered greenhouse.

Asia-Pacific demonstrates the highest 20.1% CAGR through 2030. Thailand maintains market momentum, targeting a USD 1.2 billion market value by 2025. Australia increases Special Access Scheme approvals, reducing barriers for physicians. Chinese research institutions examine low-THC hemp for industrial and pharmaceutical exports, while domestic adult-use remains restricted. South Korea initiates clinical trials under hospital oversight, indicating progressive policy changes. South America, the Middle East, and Africa present opportunities for cost-effective outdoor cultivation. Morocco's first legal harvest of 294 metric tons in 2023 demonstrates export capabilities, while South Africa's 2024 recreational legalization establishes regional development.

Competitive Landscape

The cannabis market exhibits moderate fragmentation, with the top five companies accounting for 21% of global sales. Canopy Growth Corporation maintains a 6% market share through its option-based strategy to acquire Acreage following U.S. federal reform. Tilray Brands, Inc. operates across five continents, with an annual production capacity of 210 metric tons after facility expansions. Curaleaf focuses on cash-flow management and has expanded into hemp-derived THC beverages to complement its dispensary operations. Aurora Cannabis implements a cost-leadership strategy by relocating cultivation from Alberta to Nordic facilities that meet EU-GMP export standards. Jazz Pharmaceuticals plc maintains its Epidiolex patent portfolio while researching new applications for rare seizure disorders.

In North America, companies prioritize vertical integration to manage seed-to-sale operations, while European operations require specialized partnerships due to separate distribution and cultivation licensing. Market consolidation occurs through acquisitions of distressed assets in Oregon and California, driven by price compression impacts on smaller operators. Companies improve operational efficiency through AI-enabled production systems and energy-efficient facility upgrades. Retail strategies evolve through enhanced store experiences, digital loyalty programs, and partnerships with convenience stores.

Competition intensifies around minor cannabinoid intellectual property, biosynthetic development, and ESG compliance. Companies operating carbon-neutral facilities secure agreements with pharmaceutical buyers seeking consistent, low-residue cannabis materials. Tobacco and alcohol companies maintain strategic investment positions, prepared to provide growth capital upon federal regulatory clarity. Success in the cannabis market depends on combining scientific capabilities with consumer-focused products while adapting to evolving regulations.

Cannabis Industry Leaders

-

Canopy Growth Corporation

-

Tilray Brands, Inc.

-

Curaleaf

-

Aurora Cannabis Inc.

-

Jazz Pharmaceuticals plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Green Thumb Industries reported Q1 2025 revenue of USD 280 million and outlined plans to open adult-use outlets in Minnesota.

- February 2025: Tilray Brands completed Phase I capacity expansion, lifting annual cultivation to 210 metric tons.

- February 2025: Trulieve, Curaleaf, and Green Thumb Industries released hemp-derived THC beverages targeting the USD 14 billion addressable market.

- October 2024: Canopy USA finalized the Wana acquisition, broadening edible and vape coverage.

Global Cannabis Market Report Scope

Cannabis is a tall plant with a stiff upright stem used as a drug for recreational and entheogenic purposes and is being legalized for its medical usage.

The cannabis market is segmented by product type (capsules, concentrates, edibles, and other product types), application (medical and recreational), compound type (tetrahydrocannabinol (THC), cannabidiol (CBD), and balanced THC & CBD), and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers market size and forecasts for all the above segments in value (USD).

| By Product Type | Flower | ||

| Pre-Rolls | |||

| Concentrates | |||

| Edibles | |||

| Beverages | |||

| Capsules / Soft-Gels | |||

| Topicals and Transdermals | |||

| Tinctures / Sublinguals | |||

| Other Product Types | |||

| By Application | Medical (Rx) | ||

| Adult-Use / Recreational | |||

| Wellness and Nutraceutical | |||

| By Compound Type | THC-Dominant | ||

| CBD-Dominant | |||

| Balanced THC : CBD | |||

| Minor Cannabinoids | |||

| Terpene / Flavonoid-rich Extracts | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| Czech Republic | |||

| Croatia | |||

| Rest of Europe | |||

| Asia-Pacific | Australia | ||

| China | |||

| Thailand | |||

| Rest of Asia-Pacific | |||

| South America | Argentina | ||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East | Lebanon | ||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Morocco | |||

| Ghana | |||

| Rwanda | |||

| Rest of Africa | |||

| Flower |

| Pre-Rolls |

| Concentrates |

| Edibles |

| Beverages |

| Capsules / Soft-Gels |

| Topicals and Transdermals |

| Tinctures / Sublinguals |

| Other Product Types |

| Medical (Rx) |

| Adult-Use / Recreational |

| Wellness and Nutraceutical |

| THC-Dominant |

| CBD-Dominant |

| Balanced THC : CBD |

| Minor Cannabinoids |

| Terpene / Flavonoid-rich Extracts |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| Czech Republic | |

| Croatia | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East | Lebanon |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Morocco | |

| Ghana | |

| Rwanda | |

| Rest of Africa |

Key Questions Answered in the Report

What is the projected size of cannabis market by 2030?

The market is forecast to reach USD 102.1 billion by 2030, expanding at an 18.0% CAGR from 2025 to 2030.

Which product category is projected to grow the fastest over the next five years?

Cannabis-infused beverages lead in growth, with a projected 20.6% CAGR through 2030 as large beverage and CPG companies accelerate investments.

Why is Germany viewed as pivotal to Europe’s cannabis outlook?

Germany’s Cannabis Act removed medicinal cannabis from the Narcotics Act and boosted patient numbers to nearly 900,000 by May 2025, making it Europe’s largest regulated market and a model for neighboring countries.

How does oversupply affect operators in mature North American states?

Excess production has driven wholesale prices to record lows, eroding margins, forcing bankruptcies, and spurring consolidation among vertically integrated firms.

What role do minor cannabinoids such as CBG and CBN play in future growth?

Biosynthetically produced minor cannabinoids are projected to grow at a 23.1% CAGR, offering pharmaceutical-grade purity and targeting niche therapeutic areas at premium price points.

How could U.S. federal rescheduling to Schedule III influence industry economics?

Reclassification would eliminate Section 280E tax liabilities, significantly lowering effective tax rates and improving cash flow for licensed businesses while encouraging broader banking participation.