Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

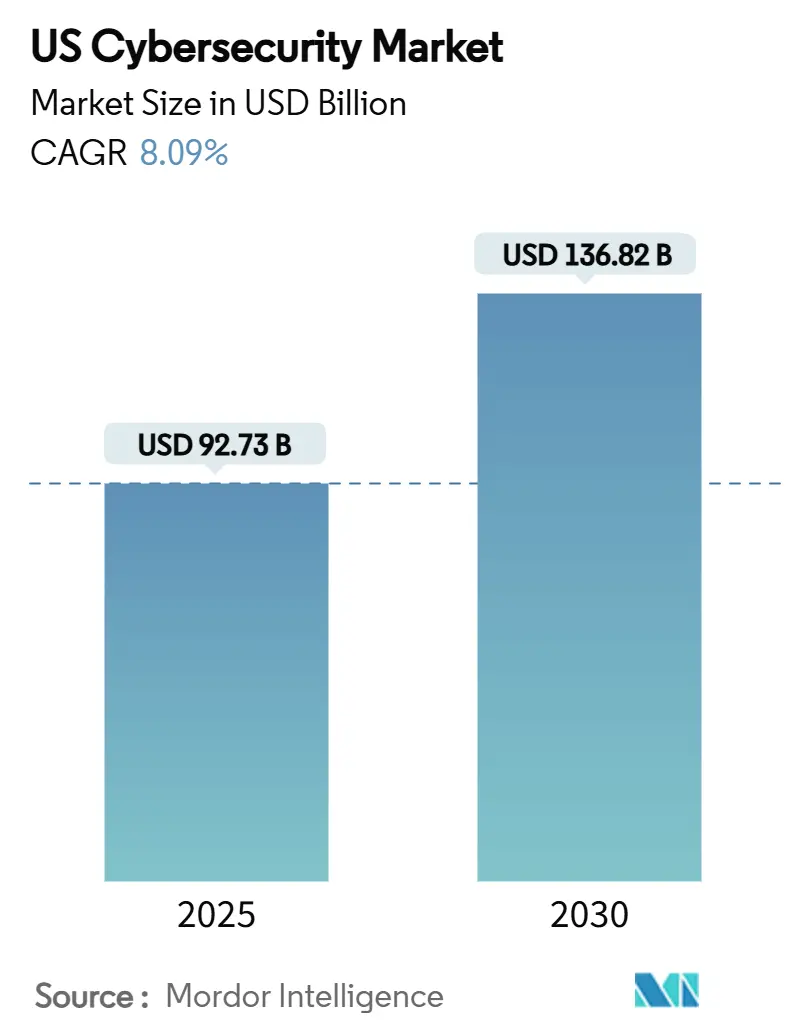

| Market Size (2025) | USD 92.73 Billion |

| Market Size (2030) | USD 136.82 Billion |

| Growth Rate (2025 - 2030) | 8.09% CAGR |

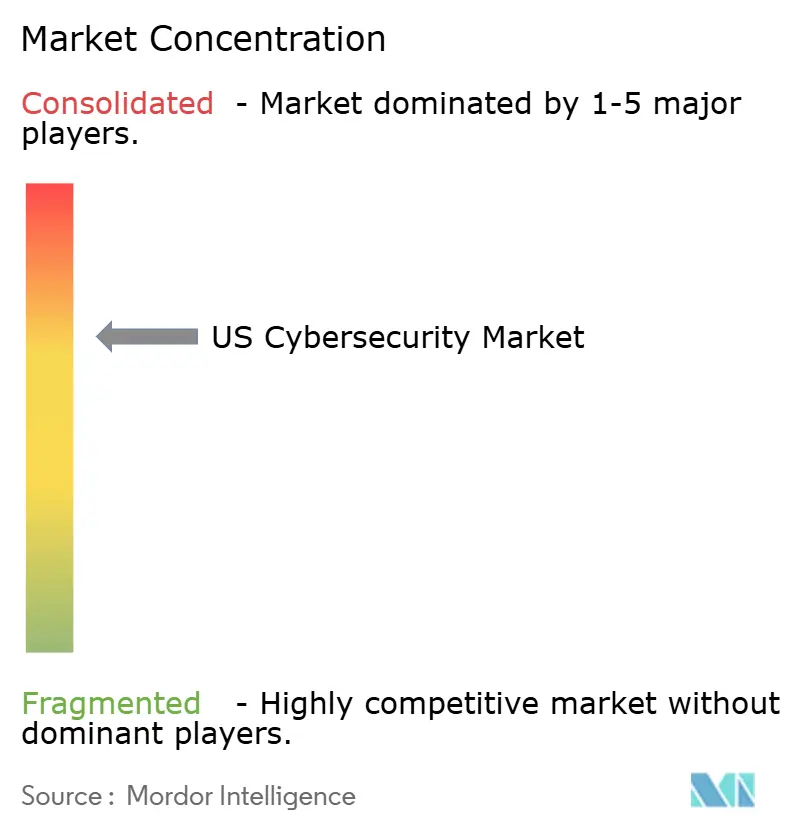

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

US Cybersecurity Market Analysis by Mordor Intelligence

The US cybersecurity market size reached USD 92.73 billion in 2025 and is projected to rise to USD 136.82 billion by 2030, reflecting an 8.09% CAGR over the forecast period. This expansion is fueled by federal zero-trust mandates, a sharp increase in ransomware attacks on critical infrastructure, and accelerated cloud migration that now places 94% of organizations in multi-cloud settings [1]Flexera, “State of the Cloud Report 2025,” flexera.com. On-premise architectures still hold the largest deployment footprint because defense, financial services, and healthcare operators retain legacy systems that must remain behind local controls; however, cloud-delivered security is advancing at a 15% CAGR as enterprises seek scalable protection and real-time threat intelligence. Venture capital continues to stimulate innovation, with USD 11.6 billion invested in US cyber start-ups during 2024, much of it channeled into AI-driven threat-detection platforms that reduce analyst workload. Mandatory SEC breach-disclosure rules, rising cyber-insurance premiums, and a persistent talent shortage collectively reinforce long-term demand, positioning the US cybersecurity market as a strategic priority for both public and private sectors.

Key Report Takeaways

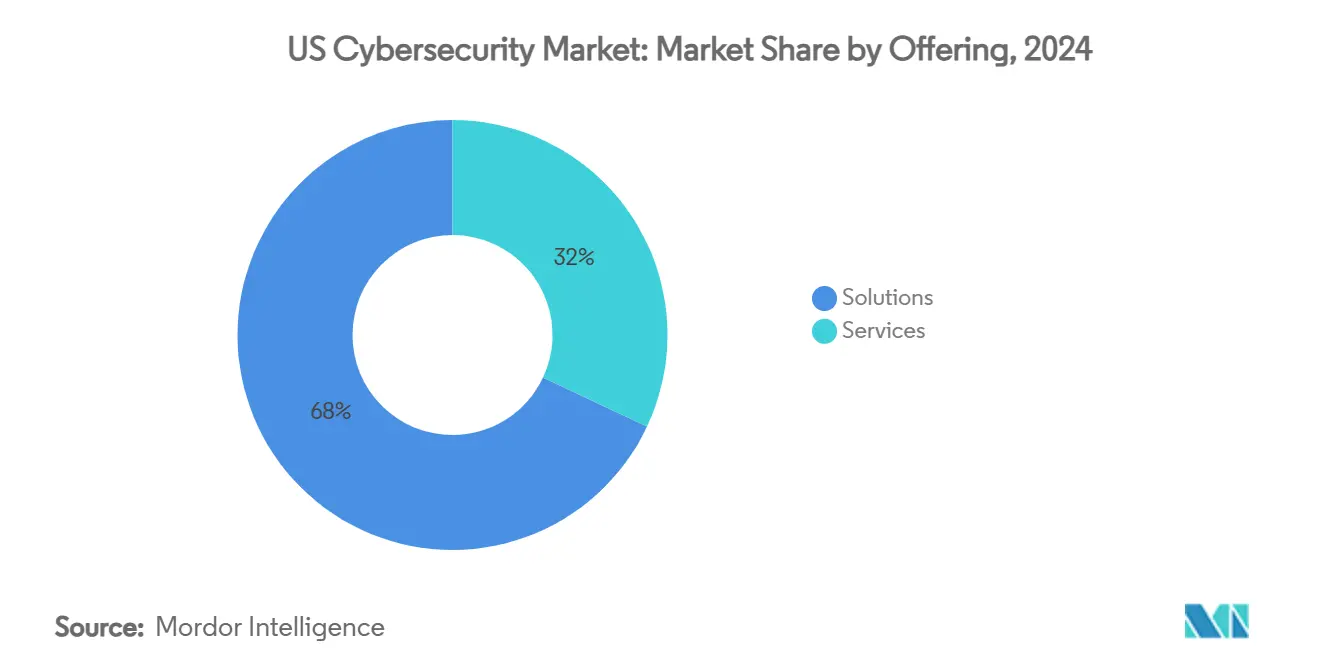

- By offering, solutions commanded 68% revenue share of the US cybersecurity market in 2024, while managed services are forecast to grow at a 15.8% CAGR to 2030.

- By deployment mode, on-premise implementations held 58% share in 2024; cloud-delivered security is advancing at a 15% CAGR through 2030.

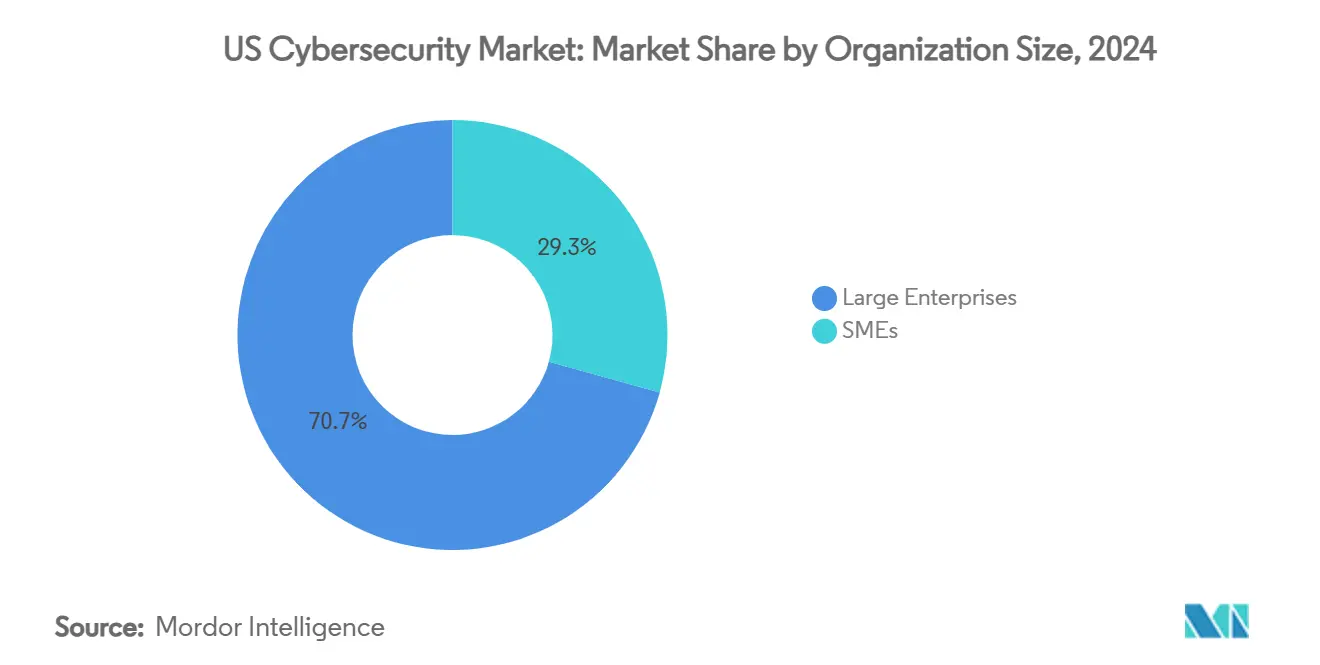

- By organisation size, large enterprises controlled 70.7% of the US cybersecurity market share in 2024, whereas SMEs are expected to expand at a 13.4% CAGR to 2030.

- By end-user vertical, BFSI led with 24% revenue share in 2024, while the healthcare segment is projected to accelerate at a 14.6% CAGR through 2030.

US Cybersecurity Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal zero-trust mandates accelerating security modernization across agencies | +1.8% | National; highest spending concentration in Washington D.C., Virginia, Maryland | Medium term (2-4 years) |

| Surge in ransomware attacks on mid-market healthcare and education institutions | +2.1% | National; pronounced in Texas, California, Florida | Short term (≤ 2 years) |

| Adoption of 5G and edge computing expanding the threat surface for critical infrastructure | +1.4% | National; early deployments in major metropolitan areas | Long term (≥ 4 years) |

| Rapid migration to SaaS and multi-cloud driving demand for cloud-native security platforms | +1.9% | National; strongest in technology hubs such as California, New York, Massachusetts | Medium term (2-4 years) |

| Venture-capital influx spurring innovation in AI-based threat-detection start-ups | +1.2% | National; venture-capital clusters in California, New York, Massachusetts | Medium term (2-4 years) |

| Escalating cyber-insurance premiums incentivizing proactive defense investments | +0.8% | National; highest effect in high-risk critical-infrastructure sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Federal Zero-Trust Mandates Accelerating Security Modernization Across Agencies

Executive Order 14028 obliges every civilian agency to adopt zero-trust architecture, triggering multi-year modernization projects that ripple through state and local governments. The Department of Homeland Security recently awarded USD 17 million to ASRC Federal for USCIS integration services, and the Treasury’s new USD 20 billion PROTECTS vehicle underscores federal buying power[2]Orange Slices, “ASRC Federal Wins USCIS Zero Trust Contract,” orangeslices.ai. Twenty-three states have published their zero-trust roadmaps, with California allocating USD 50 million for identity-centric controls across all agencies by 2026. Contractors must follow suit, extending zero-trust requirements deep into defense and financial services supply chains. The cascade effect positions the US cybersecurity market as the primary beneficiary of sustained public-sector spending.

Surge in Ransomware Attacks Targeting Mid-Market Healthcare and Education Institutions

Change Healthcare’s February 2024 breach halted prescription processing for 67,000 pharmacies and cost UnitedHealth Group USD 2.3 billion in remediation. Ascension Health faced a similar disruption three months later when a ransomware attack paralyzed electronic health-record systems across 140 hospitals. The Department of Health and Human Services confirmed that 100 million patient records were exposed last year, fueling federal pressure on hospitals to modernize defenses. Educational institutions are equally vulnerable; the FBI attributes multiple campus closures to ransomware that erased student-services databases. These events amplify spending urgency, pushing healthcare security outlays to an expected 14.6% CAGR, well above the overall US cybersecurity market trajectory.

Adoption of 5G and Edge Computing Expanding the Threat Surface for Critical Infrastructure

5G rollout embeds compute workloads at the network edge, multiplying entry points that traditional perimeter tools cannot inspect in real time. Electric utilities deploying 5G-enabled smart-grid sensors must now authenticate millions of IoT endpoints, each representing a potential foothold for nation-state actors. Verizon earmarked USD 3.2 billion in 2024 for 5G security architecture, including AI analytics that scan traffic at microsecond latency. Manufacturing facilities adopting Industry 4.0 robotics confront identical challenges, elevating demand for embedded security and edge-native protection. Consequently, long-cycle infrastructure projects ensure a durable growth engine for the US cybersecurity market.

Rapid Migration to SaaS and Multi-Cloud Driving Demand for Cloud-Native Security Platforms

Ninety-four percent of US enterprises now operate multi-cloud estates spanning an average of 2.6 providers, creating visibility gaps that legacy appliances cannot close. Microsoft’s security revenue reached USD 20 billion in fiscal 2024, with 60% of that growth attributable to cloud-native services. Hyper-scale adoption has propelled start-ups such as Wiz to USD 350 million in annual recurring revenue within four years by offering unified protection across AWS, Azure and Google Cloud. Financial institutions follow suit: JPMorgan Chase invested USD 15 billion in technology modernization in 2024, prioritizing real-time detection across hybrid workloads. This systemic pivot sustains a nearly 2-percentage-point uplift to the overall CAGR of the US cybersecurity market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented state-level privacy regulations create compliance complexity for vendors | -1.2% | National; greatest in California, Virginia, Connecticut | Medium term (2-4 years) |

| Acute talent shortage is elevating labor costs and project timelines | -1.8% | National, most acute in major technology hubs | Long term (≥ 4 years) |

| Consolidation fatigue as buyers resist multi-vendor tool sprawl | -0.9% | National, strongest among large enterprises | Short term (≤ 2 years) |

| Budget pressure on SMBs is curtailing security spend | -1.1% | National; varies with local economic conditions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented State-Level Privacy Regulations Creating Compliance Complexity for Vendors

CCPA in California, CDPA in Virginia, and CTDPA in Connecticut impose divergent breach-notification and consumer-rights requirements that force vendors to maintain state-specific compliance frameworks. The SEC’s amended Regulation S-P now obliges financial institutions to notify individuals within 30 days of a data compromise, overlapping with stricter state deadlines. Mid-market security providers report average annual compliance costs of USD 2.3 million, eroding margins, and deterring market entry. Fragmentation slows product rollouts and complicates go-to-market planning, shaving an estimated 1.2 percentage points from the US cybersecurity market CAGR.

Acute Talent Shortage Elevating Labour Costs and Project Timelines

The United States currently faces 265,000 unfilled cybersecurity positions, translating into a 28% vacancy rate across the profession. Median salaries have climbed to USD 119,000, up 15% from 2023 levels, with specialized cloud-security roles commanding even higher premiums. CISA’s USD 25 million Federal Cyber Defense Skilling Academy seeks to mitigate the shortage but requires up to two years to graduate each cohort. Enterprises respond by automating lower-level alert handling; 67% already deploy AI-powered security tooling to compensate for scarce talent. Elevated wage bills and elongated project timelines reduce purchasing flexibility, subtracting 1.8 percentage points from potential US cybersecurity market growth.

Segment Analysis

By Offering: Platform Consolidation Reinforces Solution Leadership

Solutions remain the primary revenue driver, holding 68% of the US cybersecurity market share in 2024, while managed services are forecast to grow at a 15.8% CAGR through 2030. Identity and access management adoption surged after federal zero-trust directives, and application security spending expanded alongside containerized development pipelines. Network security appliances face displacement from software-defined alternatives, whereas endpoint protection evolves toward XDR suites that ingest telemetry from laptops, servers and mobile devices. Cloud-security subcategories—particularly cloud-native application protection platforms (CNAPP)—post the fastest acceleration, reflecting multi-cloud complexity that legacy tools cannot address. Professional services hold a resilient niche in compliance audits and incident response, though the labor shortage constrains capacity and pushes billable rates higher.

Managed services growth stems from acute talent constraints and regulatory pressures that force even resource-rich enterprises to seek external expertise. MSSPs increasingly deliver security-operations-centre (SOC) functions via subscription, lowering entry thresholds for mid-market businesses. The offering mix is also shaped by tool-sprawl fatigue: 90% of large organizations run overlapping vulnerability scanners that they now seek to consolidate into integrated platforms. Vendors respond by embedding AI analytics and orchestration features, reinforcing solution stickiness and expanding average revenue per customer. Consequently, solutions retain scale, while services inject higher growth velocity into the overall US cybersecurity market.

By Deployment Mode: Cloud Momentum Outpaces Legacy Footprints

On-premises setups accounted for 58% of revenue in 2024, largely because defence, financial-services and healthcare sectors must preserve data sovereignty and legacy integrations. Federal agencies continue to maintain classified networks behind air-gapped environments, although analytics layers increasingly migrate to commercial clouds. Financial institutions such as JPMorgan Chase invest in hybrid architecture that combines on-premises key-management with cloud-native detection, ensuring regulatory compliance without sacrificing agility.

Cloud-delivered security solutions expanded at a 15% CAGR, buoyed by reduced capital spending, elastic scaling and the speed of software-as-a-service rollouts. Organizations deploying SECaaS report implementation cycles 40% shorter than appliance-based alternatives, accelerating time to risk reduction. Providers integrate threat-intelligence feeds and behavioral analytics, delivering a continuously updated control plane that adapts to evolving attacker techniques. The growth differential widens the revenue gap over time, causing the on-premises slice of the US cybersecurity market to contract in relative terms, even as absolute spending remains stable in compliance-heavy industries.

By Organization Size: Enterprise Spend Dominates While SME Adoption Quickens

Large enterprises represented 70.7% of 2024 revenue, sustaining high ticket sizes and multi-year platform contracts. Fortune 500 companies operate complex global footprints that demand round-the-clock SOC coverage, zero-trust enforcement and granular identity governance. Their procurement leverage allows volume discounts across bundled licences, but tool proliferation elevates maintenance overhead and fuels renewed appetite for integrated suites.

SMEs record a 13.4% CAGR to 2030, reflecting heightened threat exposure and tightening regulatory scrutiny that no longer exempts smaller entities. Ransomware gangs increasingly pivot to mid-market targets lacking dedicated security staff, prompting boards to allocate funds despite tight IT budgets. Managed services and cloud-delivered controls lower barriers by shifting expenditure to operating-expense models. Vendor roadmaps now feature simplified dashboards and guided policy templates tuned to SME resource constraints, ensuring the cohort becomes a rising contributor to US cybersecurity market expansion.

By End-User Vertical: BFSI Retains Scale as Healthcare Leads Growth

BFSI captured 24% of 2024 revenue, underpinned by SEC disclosure rules, Federal Financial Institutions Examination Council guidelines and real-time payment fraud risks. Banks deploy AI-assisted graph analytics to correlate transaction anomalies across millions of events per second, while insurers add behavioral biometrics to reduce account-takeover losses. High-value data makes the sector an ongoing priority for nation-state and organized-crime groups, ensuring that cybersecurity budgets remain non-discretionary.

Healthcare’s 14.6% CAGR is unmatched, driven by the operational chaos inflicted by recent ransomware incidents. Hospital administrators now prioritize network segmentation, immutable backups and legacy system upgrades to safeguard patient safety. The Department of Health and Human Services has signaled stricter minimum-capability expectations, further reinforcing spending momentum. Telecommunications, manufacturing, and energy also expand, propelled by 5G, Industry 4.0, and smart-grid adoption, though at rates closer to the broader US cybersecurity market size trajectory.

Geography Analysis

Regional demand clusters around federal spending in the Washington D.C. corridor, venture-capital inflows in California and financial-services concentration in New York. California leads absolute outlays, amplified by USD 11.6 billion of start-up funding in 2024 and 1,338 reported breaches that sharpen corporate risk perception[3]Identity Theft Resource Center, “US 2024 Annual Breach Report,” identitytheftresourcecenter.org.

New York commands 28% of nationwide cybersecurity budgets owing to its dense population of banks and capital markets firms that must comply with NYDFS Part 500. The mid-Atlantic benefits from Treasury’s USD 20 billion PROTECTS vehicle and other large federal frameworks, steering vendor headquarters and talent pools toward Northern Virginia and Maryland.

Texas exhibits double-digit growth as energy, healthcare and defence installations adopt zero-trust and operational-technology security, collectively driving a 12.3% annual expansion. Florida gains momentum from emerging fintech hubs in Miami and Tampa, supported by state incentives that attract cyber start-ups. The Midwest shows steady uptake as automotive plants in Michigan deploy OT-security for connected production lines, while Ohio manufacturers integrate 5G sensors that require edge-native protection. Even remote regions such as Alaska demonstrate disproportionate breach volumes—319 incidents per 100,000 residents—showing that exposure transcends geography and sustaining nationwide relevance for the US cybersecurity market.

Competitive Landscape

Seven incumbent platform vendors collectively account for more than 65% of revenue, with Palo Alto Networks leading at roughly 9%, followed by CrowdStrike, Fortinet, Cisco, Microsoft, Check Point and Zscaler. Consolidation reflects buyer demand for unified suites that reduce operational complexity and licensing overhead. Strategic acquisitions accelerate feature convergence:

Palo Alto Networks added Protect AI for model-security capabilities, while CrowdStrike expanded cloud posture management via Bionic. Microsoft integrates proprietary threat intelligence and identity protection into its E5 license bundle, leveraging enterprise licensing to deepen lock-in.

Venture capital infuses agility into the ecosystem, backing cloud-native and AI-centric challengers. Prophet Security closed an USD 11 million Series A to automate threat-hunting workflows, and Wiz surpassed USD 350 million in ARR by focusing solely on multi-cloud application security. Identity-centric specialists such as CyberArk grow by addressing privileged-access gaps, while government-focused providers like Zscaler Federal capture zero-trust spending. The competitive dynamic therefore balances scale economics of major platforms against rapid innovation cycles of emergent start-ups, sustaining healthy rivalry within the US cybersecurity market.

US Cybersecurity Industry Leaders

-

IBM Corporation

-

Cisco Systems Inc

-

Dell Technologies Inc.

-

Fortinet Inc.

-

Intel Security (Intel Corporation)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: The US Department of the Treasury awarded 10 spots on a USD 20 billion PROTECTS Cyber Support BPA, signaling unprecedented financial-sector resilience investment.

- November 2024: Ultraviolet Cyber secured the US Agency for Global Media Zero Trust Architecture Services contract, prevailing over 20 bidders and underscoring federal zero-trust intensity.

- September 2024: ASRC Federal won a USD 17 million USCIS Zero Trust Integration Services award, accelerating agency compliance with Executive Order 14028.

- September 2024: Coalfire Federal obtained the NIH NHLBI Cybersecurity Risk Management Framework task, highlighting healthcare security investment.

US Cybersecurity Market Report Scope

Cybersecurity solutions help an organization to monitor, detect, report, and counter cyber threats that are internet-based attempts to damage or disrupt information systems and hack critical information using spyware and malware, and by phishing, to maintain data confidentiality.

The United States cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Solutions | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Solutions | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By Organization Size

| SMEs |

| Large Enterprises |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail |

| Energy and Utilities |

| Manufacturing |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected growth of the US cybersecurity market?

The market is forecast to rise from USD 92.73 billion in 2025 to USD 136.82 billion by 2030, registering an 8.09% CAGR.

Which offering currently generates the most revenue?

Solutions hold 68% of 2024 revenue, while managed services show the fastest momentum at a 15.8% CAGR through 2030.

How are federal zero-trust mandates affecting spending?

Executive Order 14028 has sparked large awards such as the Treasury’s USD 20 billion PROTECTS BPA and prompted 23 states to publish their own zero-trust roadmaps, lifting nationwide demand.

Which end-user vertical is expanding the quickest?

Healthcare security outlays lead with a 14.6% CAGR after ransomware events at Change Healthcare and Ascension Health exposed critical vulnerabilities.

Why does the cybersecurity talent shortage act as a market restraint?

The country has 265,000 unfilled roles, driving median salaries to USD 119,000 and lengthening project timelines, which deters some investments.

How concentrated is vendor market share?

Seven leading providers control just over 65% of US revenue, giving the industry a concentration score of 7 on a 10-point scale.

Page last updated on: